Stock concentration is a key concern in the selection of the appropriate index. An index that has a high degree of stock concentration or a low effective number of stocks may be relatively undiversified.

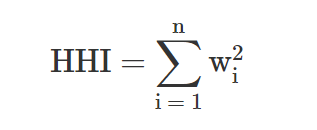

Concentration can be captured using the concept of “effective number of stocks,” which can be measured using the Herfindahl-Hirschman index (HHI). HHI is the sum of the squared weights of the individual stocks in the portfolio:

where:

n = the number of stocks in the portfolio

wi = the weight of stock i

HHI ranges from ¹/ₙ (an equally-weighted portfolio) to 1 (a single stock portfolio), so as HHI increases, concentration risk increases. The effective number of stocks is the reciprocal of the HHI:

A market-cap weighted index with 500 stocks might have an HHI of 0.01 and, therefore, an effective number of stocks of ¹/₀.₀₁ = 100. The fact that 100 is less than the number of stocks in the portfolio reflects the disproportionate effect of the largest capitalization stocks on the index.

An equal weighted index of 500 stocks would have an HHI of 0.002 and an effective number of stocks of ¹/₀.₀₀₀₂ = 500.