The CFA can give us 4 different financial statement items and expect us to make the appropriate adjustments to get to FCFF. From there we can get to FCFE, or we can also start with 2 different line items and go right to FCFE.

The first line item is Net Income. FCFF can be calculated with the following adjustments to NI:

FCFF = NI + NCC + [Int × (1 − tax rate)] − FCInv – WCInv

where:

NI = net income

NCC = noncash charges

Int = interest expense

FCInv = fixed capital investment (capital expenditures)

WCInv = working capital investment

NCC or non-cash charges is generally depreciation, amortization of intangibles, deferred taxes

FCInv is fixed capital investment or capex, which can be found by determining the increase in gross fixed assets. If there are proceeds from the sale of long-term assets, that is subtracted from the FCInv, as that would be a cash inflow.

- Simple FCInv (No Asset Sale) = ending net PP&E – beginning net PP&E + depreciation

- Simple FCInv (No Asset Sale) = ending net PP&E – beginning net PP&E + depreciation – gain/loss from asset sale

- FCInv = capital expenditures − proceeds from sales of long-term assets

WCInv is change in working capital, excluding cash and cash like assets.

- WCInv = Increase in accounts receivable + Increase in inventory – Increase in accounts payable – Increase in accrued liabilities

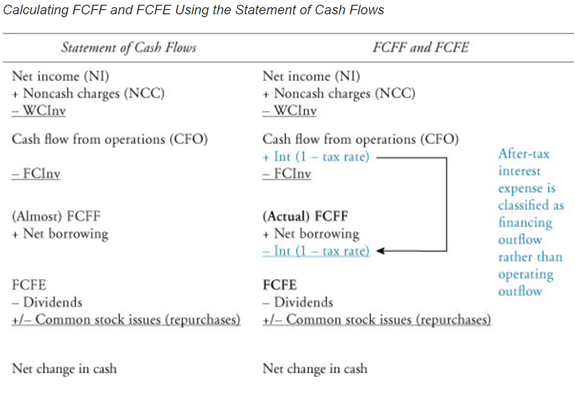

Interest was expensed on the income statement, but it represents a financing cash flow to bondholders that is available to the firm before it makes any payments to its capital suppliers. Therefore, we have to add it back. However, we don’t add back the entire interest expense, only the after-tax interest cost because paying interest reduces our tax bill.

FCFF Calculations:

- FCFF = NI + NCC + Int(1 – Tax rate) – FCInv – WCInv

- FCFF = CFO + Int(1 – Tax rate) – FCInv

- FCFF = EBIT(1−Tax rate) + Dep – FCInv – WCInv

- FCFF = EBITDA(1 – Tax rate) + Dep(Tax rate) – FCInv – WCInv

FCFE Equations:

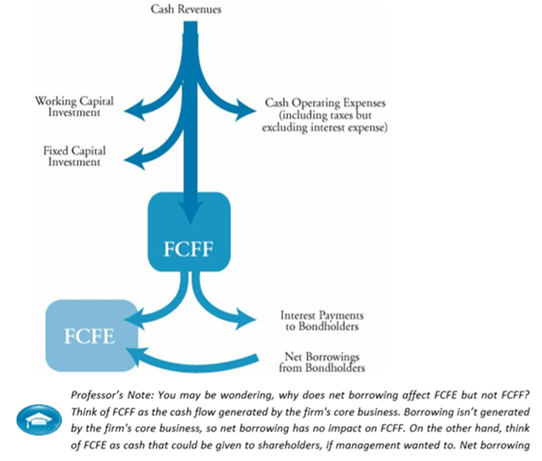

- FCFE = NI + NCC – FCInv – WCInv + Net borrowing

- FCFE = FCFF − Int(1 – Tax rate) + Net borrowing

- FCFE = CFO – FCInv + Net borrowing

- FCFE= EBIT(1 – Tax rate) + Dep − Int(1−Tax rate) – FCInv – WCInv + Net borrowing

- FCFE = EBITDA(1 – Tax rate) + Dep(Tax rate) − Int(1 – Tax rate) – FCInv – WCInv + Net borrowing

- FCFE = Net income − (1−DR)(Capital expenditures − Depreciation) − (1 − DR)(WCInv)

- DR = constant debt ratio