Monetary Policy

Monetary policy is often used as a mechanism for intervention in the business cycle. The common theme is that central banks virtually always aim to moderate the cyclical behavior of growth and inflation, in both directions. Thus, monetary policy aims to be countercyclical.

Most central banks strive to balance price stability against economic growth. The ultimate goal is to keep growth near its long-run sustainable rate, because growth faster than the long-run rate usually results in increased inflation. As discussed previously, the later stages of an economic expansion are often characterized by increased inflation. As a result, central banks usually resort to restrictive policies toward the end of an expansion. The risk at this stage is that they may overtighten and cause a recession.

To spur growth, a central bank can take actions to reduce short-term interest rates. This results in greater consumer spending, greater business spending, higher stock prices, and higher bond prices. Lower interest rates also usually result in a lower value of the domestic currency, which is thought to increase exports.

The neutral rate is the rate that most central banks strive to achieve as they attempt to balance the risks of inflation and recession. If inflation is too high, the central bank should increase short-term interest rates. If economic growth is too low, it should decrease interest rates. The Taylor rule embodies this concept. Thus, it is used as a prescriptive tool (i.e., it states what the central bank should do). It also is fairly accurate at predicting central bank action.

Negative Interest Rates

A negative rate is defined as a net payment made to keep money on deposit at a financial institution or payment of a net fee to invest in short-term instruments.

Key considerations when forming capital market expectations in a negative interest rate environment include the following:

- Historical data are less likely to be reliable.

- Useful data may exist on only a few historical business cycles, which may not include instances of negative rates. In addition, fundamental structural/institutional changes in markets and the economy may have occurred since this data was generated.

- Quantitative models, especially statistical models, tend to break down in situations that differ from those on which they were estimated/calibrated.

- Forecasting must account for differences between the current environment and historical averages. Historical averages, which average out differences across phases of the cycle, will be even less reliable than usual.

- The effects of other monetary policy measures occurring simultaneously (e.g., quantitative easing) may distort market relationships such as the shape of the yield curve or the performance of specific sectors.

Fiscal Policy

Another tool at the government’s disposal for managing the economy is fiscal policy. If the government wants to stimulate the economy, it can implement loose fiscal policy by decreasing taxes or increasing spending, thereby increasing the budget deficit. If they want to rein in growth, the government does the opposite to implement fiscal tightening.

There are two important aspects to fiscal policy. First, it is not the level of the budget deficit that matters—it is the change in the deficit. For example, a deficit by itself does not stimulate the economy, but increases in the deficit are required to stimulate the economy. Second, changes in the deficit that occur naturally over the course of the business cycle are not stimulative or restrictive.

Fiscal policy is inherently political. Central banks ultimately derive their powers from governments, but most strive to be, or at least appear to be, independent of the political process in order to maintain credibility. Fiscal policy typically addresses objectives other than regulating short-term growth because:

- The fiscal decision-making process is too lengthy to make timely adjustments to aggregate spending and taxation aimed at short-term objectives.

- Frequent changes of a meaningful magnitude would be disruptive to the ongoing process of providing and funding government services.

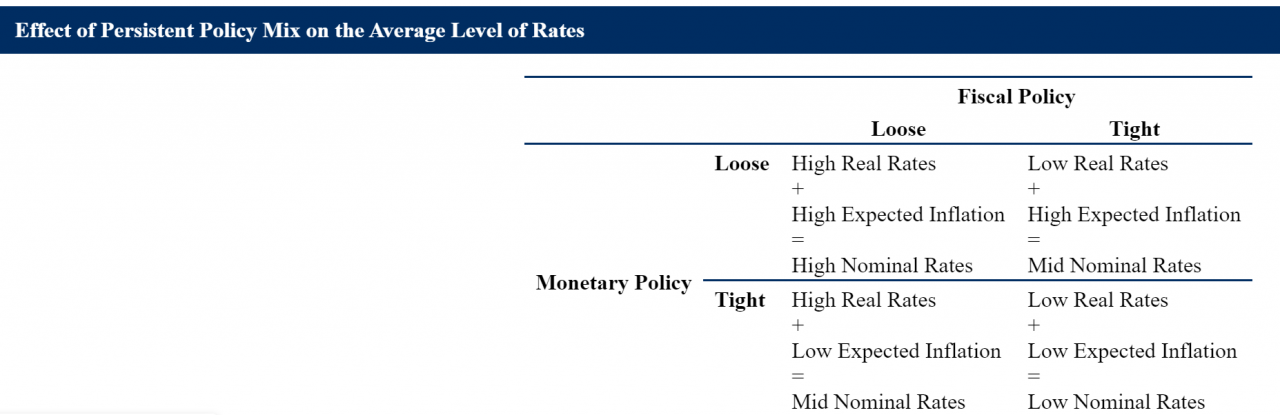

The Monetary and Fiscal Policy Mix

The mix of monetary and fiscal policies has its most apparent impact on the level of interest rates and the shape of the yield curve.

Exhibit 6. Rates, Policy, and the Yield Curve over the Business Cycle

| Cycle Phase | Monetary Policy & Automatic Stabilizers | Money Market Rates | Bond Yields and the Yield Curve |

|---|---|---|---|

| Initial Recovery | Stimulative stance. Transitioning to tightening mode. | Low/bottoming. Increases expected over progressively shorter horizons. | Long rates bottoming. Shortest yields begin to rise first. Curve is steep. |

| Early expansion | Withdrawing stimulus | Moving up. Pace may be expected to accelerate. | Yields rising. Possibly stable at longest maturities. Front section of yield curve steepening, back half likely flattening. |

| Late expansion | Becoming restrictive | Above average and rising. Expectations tempered by eventual peak/decline. | Rising. Pace slows. Curve flattening from longest maturities inward. |

| Slowdown | Tight. Tax revenues may surge as accumulated capital gains are realized. | Approaching/reaching peak. | Peak. May then decline sharply. Curve flat to inverted. |

| Contraction | Progressively more stimulative. Aiming to counteract downward momentum. | Declining. | Declining. Curve steepening. Likely steepest on cusp of Initial Recovery phase. |