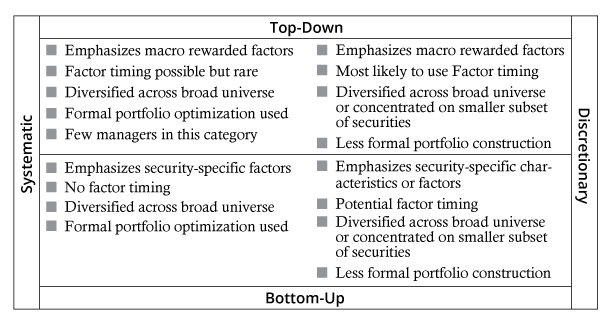

A manager’s portfolio construction process should reflect her beliefs with respect to the nature of her skills in each of these areas. The majority of investment approaches can be classified as either

- systematic or discretionary – the degree to which a portfolio construction process is subject to a set of predetermined rules or is left to the discretionary views of the manager

and

- bottom-up or top-down – the degree to which security-specific factors, rather than macroeconomic factors, drive portfolio construction

Each manager’s investment approach is implemented within a framework that specifies the acceptable levels of active risk and active share relative to a clearly articulated benchmark. (Active Share is a measure of how similar a portfolio is to its benchmark.) A manager may emphasize these dimensions to varying degrees as he attempts to differentiate his portfolio from the benchmark.

Approaches and Their Use of Building Blocks

There are two measures of benchmark-relative risk used to evaluate a manager’s success—Active Share and active risk—and they do not always move in tandem. A manager can pursue a higher Active Share without necessarily increasing active risk (and vice versa).

The Implementation Process: The Objectives and Constraints

The simplest conceptual way to think about portfolio construction is to view it as an optimization problem. A standard optimization problem has an objective function and a set of constraints. The objective function defines the desired goal while the constraints limit the actions one can take to achieve that goal. Portfolio managers are trying to achieve desirable outcomes within the bounds of permissible actions.

Objective Functions and Constraints of Portfolio Construction

| Absolute Framework | Relative Framework | |

|---|---|---|

| Objective Function | Maximize Sharpe Ratio | Maximize Information Ratio |

| Constraints | ||

| Sector/security weights | Maximum size in portfolio | Maximum deviation from benchmark |

| Risk | Maximum portfolio volatility specified as multiple (e.g., 0.9) of benchmark volatility | Maximum tracking error (active risk) |

| Market capitalization | Maximum/minimum set by mandate | Maximum/minimum set by mandate |

Other approaches to optimization include:

- Specifying objectives in terms of risk

- Maximizing exposure to rewarded factors

- Maximizing exposure to securities having specific characteristics custom-defined by a discretionary manager

- Heuristic approaches that use less scientific methods, such as basing weighting on the ranking of securities with respect to a specified desired characteristic