Traditional finance is grounded in neoclassical economics. Within traditional finance, individuals are assumed to be risk-averse, self-interested utility maximizers. Investors who behave in a manner consistent with these assumptions are referred to as rational.

Behavioral finance is largely grounded in psychology. The term behavioral finance—generally defined as the application of psychology to finance—appears regularly in books, magazine articles, and investment papers; however, a common understanding of what is meant by behavioral finance is lacking.

Behavioral finance recognizes that the way information is presented can affect decision-making, leading to both emotional and cognitive biases.

- Cognitive errors. Errors resulting from faulty information processing or memory. These often arise from the brain’s attempt to simplify information processing.

- Emotional bias. Errors resulting from the priority of human emotions over rational decision-making. Emotions such as joy, hate, fear, and love may result in decision-making that differs from a rational, dispassionate approach.

Traditional Finance

Traditional finance is based on neoclassical economics and assumes individuals are risk-averse, have perfect information, and focus on maximizing their personal utility function.

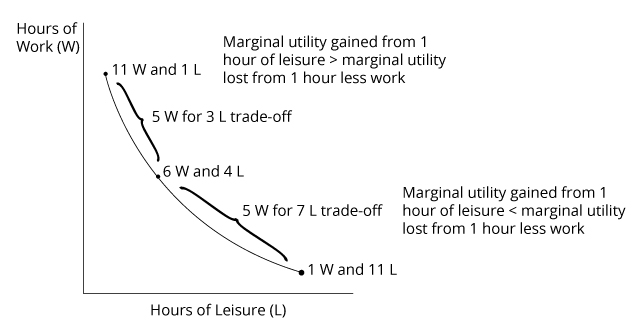

A rational investor will exhibit utility theory, which asserts individuals have a limited budget and will select the mix of goods and services that maximize their utility.

Traditional finance assumes that after gathering information and analyzing it according to Bayes’ formula, individuals will make decisions consistent with the decisions of homo economicus or rational economic man (REM)

Traditional finance is based in utility theory with an assumption of diminishing marginal utility.

Trade-Off Between Work and Leisure

The basic axioms of utility theory are completeness, transitivity, independence, and continuity.

- Completeness assumes that an individual has well-defined preferences and can decide between any two alternatives.

- Transitivity assumes that, as an individual decides according to the completeness axiom, an individual decides consistently.

- Independence also pertains to well-defined preferences and assumes that the preference order of two choices combined in the same proportion with a third choice maintains the same preference order as the original preference order of the two choices.

- Continuity assumes there are continuous (unbroken) indifference curves such that an individual is indifferent between all points, representing combinations of choices, on a single indifference curve.

A REM, when presented with new information, is assumed to adapt his beliefs about probabilities using Bayes’ formula.

Bayes’ formula shows how one conditional probability is inversely related to the probability of another mutually exclusive outcome. The formula is:

- P(A|B) = [P(B|A)/P(B)] P(A)

where:

P(A|B) = conditional probability of event A given B. It is the updated probability of A given the new information B.

P(B|A) = conditional probability of B given A. It is the probability of the new information B given event A.

P(B) = prior (unconditional) probability of information B.

P(A) = prior probability of event A, without new information B. This is the base rate or base probability of event A.

In a perfect world, when people make decisions under uncertainty, they are assumed to do the following:

- Adhere to the axioms of utility theory.

- Behave in such a way as to assign a probability measure to possible events.

- Incorporate new information by conditioning probability measures according to Bayes’ formula.

- Choose an action that maximizes the utility function subject to budget constraints (consistently across different decision problems) with respect to this conditional probability measure.

Expected utility theory generally assumes that individuals are risk-averse. This means that an individual may refuse a fair wager (a wager with an expected value of zero), and also implies that his utility functions are concave and show diminishing marginal utility of wealth.

Given two choices—investing to receive an expected value with certainty or investing in an uncertain alternative that generates the same expected value—someone who prefers to invest to receive an expected value with certainty rather than invest in the uncertain alternative that generates the same expected value is called risk-averse.

Risk-averse. The risk-averse person suffers a greater loss of utility for a given loss of wealth than they gain in utility for the same rise in wealth.

Risk-neutral. The risk-neutral person gains or loses the same utility for a given gain or loss of wealth.

Risk seeker. The risk-seeking person gains more in utility for a rise in wealth than they lose in utility for an equivalent fall in wealth.

Behavioral Finance

The validity of rational economic man (REM) has been the subject of much debate since the model’s introduction. Those who challenge REM do so by attacking the basic assumptions of perfect information, perfect rationality, and perfect self-interest.

Behavioral finance observes that individuals sometimes exhibit risk-seeking as well as risk-averse behavior. Many people simultaneously purchase low-payoff, low-risk insurance policies (risk-averse behavior) and low-probability, high-payoff lottery tickets (risk-seeking behavior).

Combinations of risk seeking and risk aversion may result in a complex double inflection utility function.

Bounded rationality assumes knowledge capacity limits and removes the assumptions of perfect information, fully rational decision-making, and consistent utility maximization. Individuals instead practice satisfice.

Limitations imposed by cost and time result in outcomes that offer sufficient satisfaction rather than optimal utility. Individuals operate with partial information and use heuristics (mental shortcuts) to process the information.

Prospect theory further relaxes the assumption of risk aversion and instead proposes loss aversion. Prospect theory is suited to analyzing investment decisions that involve risky outcomes. It focuses on the framing of decisions as either gains or losses and weighting uncertain outcomes. While utility theory assumes risk aversion, prospect theory assumes loss aversion. Loss aversion bias is where individuals fear losses more than they value gains.

| Traditional Finance Assumes: | Bounded Rationality* and Prospect Theory** Assume: |

|---|---|

| Unlimited perfect knowledge | Capacity limitations on knowledge* |

| Utility maximization | Satisfice* |

| Fully rational decision-making | Cognitive limits on decision-making* |

| Risk aversion | Reference dependence to determine gain or loss leading to possible cognitive errors** |