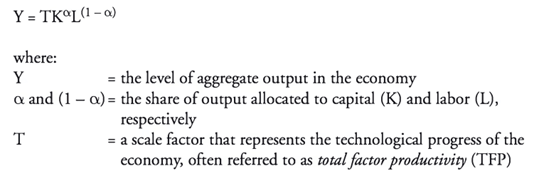

Cobb-Douglas Function

The Cobb-Douglas Function states that GDP is a function of labor and capital inputs, and their respective productivity. The model is shows constant returns to scale, in that increase all inputs by a percentage will lead to an equal percentage increase in output.

While the model incorporates diminishing returns to capital, increase in total factor productivity can shift the productivity curve upward.

Classical Growth Theory

The classical growth theory states that there is a steady state level of GDP per capita, and any growth in real GDP is only temporary. The growth will cause a population boom and GDP per capita will return to subsistence level.

Neoclassical Growth Theory

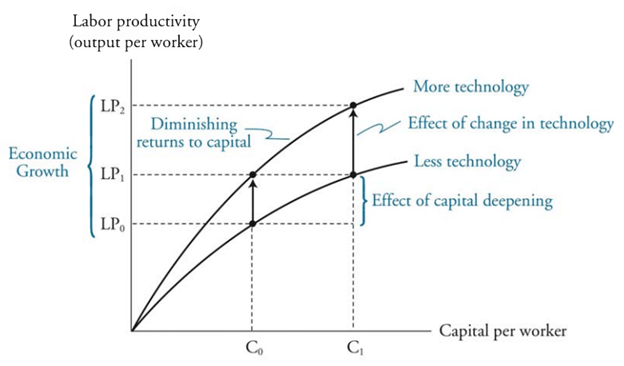

Neoclassical theory suggests that the sustainable growth rate of an economy is a function of population growth, labor’s share of income and the rate of technological advancement.

Growth gained from other factors can increase the growth rate for the short term but are temporary gains. This includes savings and non-technologically driven improvements to capital productivity, or capital deepening.

Economies will move to steady state regardless of initial capital to labor ratio of level of technology. Investments in capital which have diminishing returns.

Neoclassical theory assumes diminishing returns on investments in capital and notes that technological progress can preempt diminishing returns by shifting an economy’s TFP. However, this growth comes form exogenous improvements in TFP.

Endogenous Growth Theory

In the Endogenous Growth Theory, investment in capital has constant returns, and this allows for permanent increase in growth rates that are linked to the savings rate. There is no steady state growth rate.