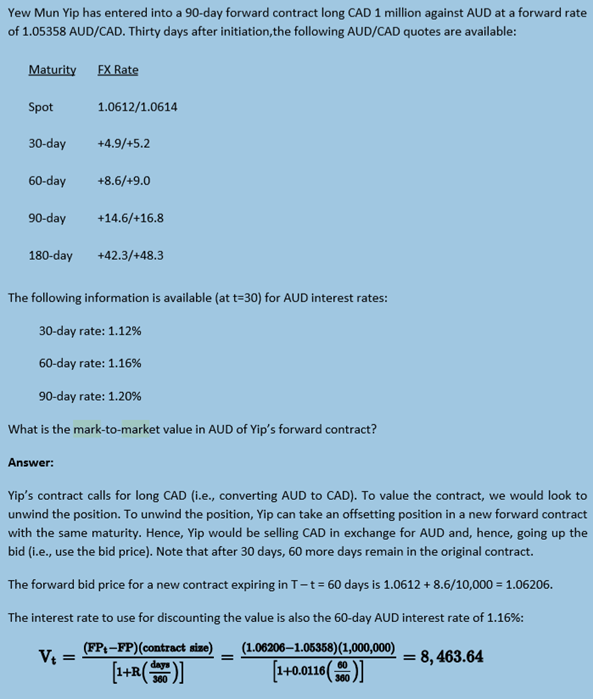

Mark-to-Market

An application of the forward rate valuation equation is the calculating the mark-to-market value of a forward currency contract. The mark-to-market value of the contract is the value one party would be willing to pay to exit the contract at the current time, before the contract expires.

Conceptually, the contract has a long and short position. The party that wants to hedge P currency risk will sell a P currency against their home currency B with a currency contract. In practice, to exit that contract early, the party that’s hedging P currency risk would purchase a new contract with the same expiration, but buy currency P. The present value of difference between the two contracts would be the mark-to-market value.

To obtain the current contract price at time t, we need to take the original spot rate and add the points to the offer price in this case, as we are buying the currency to exit the position. The points will for the time remaining on the contract, and will often be given in the exam. The rate we use to discount will be the interest rate of currency B, which is our domestic currency, annualized by the number of day remaining on the contract.