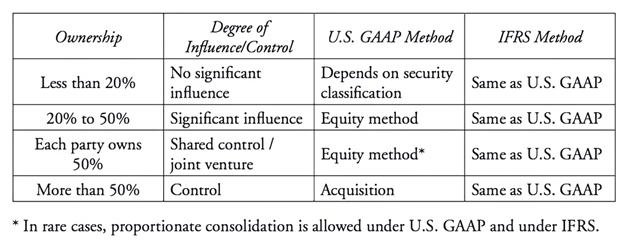

Reporting of Intercorporate Investments

Reporting of intercorporate investments depends on the percent of ownership in the investee. There are four ownership levels, less than 20%, 20-50%, 50/50, and more than 50%. The categories are determined by the significance of influence exerted by the investor over the investee.

Based on the level of ownership and influence we can us the Financial Asset, Equity or Acquisition Method to account for these investments.

Financial Assets

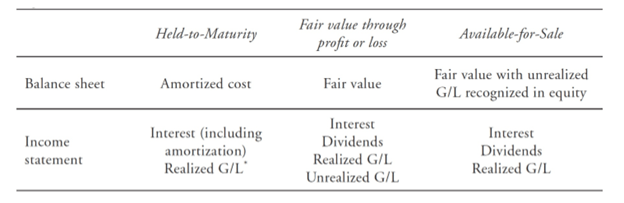

When investment ownership is less than 20% we record the acquisition of the financial asset at cost and dividend/interest income is recognized on the income statement. Changes in the value of the securities will be recorded based on how the security is classified.

Unique to debt securities is the held-to-maturity classification. These are reported initially at amortized/historical cost (discounted PV of future cash flows) and interest income is recognized on the income statement. No changes in fair value adjustments are recognized.

Fair Value Through Profit and Loss securities can be accounted for as held-for-trading or designated at fair value. Held-for-trading are securities meant for short-term profit opportunities and are reported initially at fair value. Changes in fair value as well as dividend/interest payments are all recognized in the income statement. Under the FVTPLS designation, we also have designated-at-fair value securities. They are accounted for the same as held for trading securities.

Available-for-sale securities are neither held-to-maturity or held for trading. They are initially reported at fair value, but only realized gains and losses are reported. Dividend and interest income, along with the realized gains or losses are reporting on the income statement. Unrealized gains and losses are reporting in shareholder’s income under OCI, and adjusted when the security is sold into realized cash.

Reclassification rules for Financial Assets

Securities cannot be reclassified as designation as Fair Value is irrevocable. Reclassification of debt from held for trading to FV is permitted under business model changes.

Equity Method

Under Equity Method investments, investment is listed at cost. Dividends paid effect cash levels on the balance sheet and are balanced by a decrease in investment account. On the income statement, only the pro-rata share of investee’s net income is recognized.

Acquisition Method

Under the acquisition method, balance sheets and income statements are consolidated.