With the introduction of volatility futures and variance swaps, many investors now consider volatility an asset class in itself. In particular, long volatility exposure can be an effective hedge against a sell-off in a long equity portfolio, notably during periods of extreme market movements

Volatility Futures and Options

The best know measure of market volatility is the CBOE Volatility Index (more commonly known as VIX). The VIX Index measures implied volatility in the S&P 500 Index over a forward period of 30 days.

VIX computes a weighted average of implied volatility inferred from S&P 500 traded options (calls and puts) with an average expiration of 30 days. The VIX is not a measure of actual volatility but rather the expected volatility that is priced into options.

VIX is also known as the fear index or fear gauge as we can directly view the market’s expectations of future volatility.

The VIX futures price can be interpreted as the expected S&P 500 Index volatility in the 30-day period after the futures contract expiration date.

| Position | Term Structure | Roll Yield |

|---|---|---|

| Long futures position | Contango | Negative |

| Short futures position | Contango | Positive |

| Long futures position | Backwardation | Positive |

| Short futures position | Backwardation | Negative |

VIX options are cash-settled European-style options. VIX options can only be exercised at contract maturity; therefore, the value of the option is determined by the expectations of VIX at the contract expiry. VIX call options will gain in value if expectations of volatility at maturity of the option increase, and put options will gain in value if expectations of volatility fall.

Variance Swaps

Variance swaps are instruments used by investors for taking directional bets on implied versus realized volatility for speculative or hedging purposes. The term “variance swap” refers to the fact that these instruments have a payoff analogous to that of a swap.

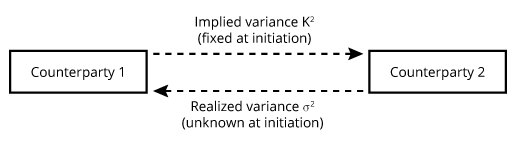

These products are termed swaps as they have two counterparties, one making a fixed payment and the other making a variable payment. The fixed payment is typically based on implied volatility2 (implied variance) over the period and is known at the initiation of the swap; this is referred to as the variance strike. The variable payment is unknown at swap initiation and is only known at swap maturity. It is the actual variance of the underlying asset over the life of the swap and is referred to as realized variance (σ2).

There is no exchange of notional principal at the initiation of the swap. A variance swap also has no interim settlement periods. With a variance swap, there is a single payment at the expiration of the swap based on the difference between actual and implied variance over the life of the swap:

settlement amountT = (variance notional)(realized variance − variance strike)

The value of the swap is zero at initiation because implied volatility is the best ex ante estimate of realized volatility.

Long (purchaser) describes the counterparty who receives the realized variance (actual) and pays the swap’s variance strike (implied volatility).

| Realized volatility | > | strike | Buyer (long) of swap makes a profit |

| Realized volatility | < | strike | Buyer (long) of swap makes a loss |

Realized variance is calculated by taking the natural log of the daily price relatives, the closing price on day t, divided by the closing price on day t − 1:

Ri = ln(Pt / Pt–1)

Because the payoffs on a variance swap are based on variance, while the strike price is expressed in terms of volatility, the payoffs for a variance swap are convex with respect to volatility. Compared to the payoffs on a volatility derivative with payoffs that are linear with respect to volatility, (1) when realized volatility is below the strike, the losses on the variance swap are smaller than the losses on the volatility derivative, and (2) when realized volatility is above the strike, the gains on the variance swap are greater than the gains on the volatility derivative. This convexity is similar in nature to the convexity of bond prices with respect to yield. With the variance swap, payoffs are increasing at an increasing rate when volatility rises and decreasing at a decreasing rate when volatility falls.

Convexity is an attractive feature to those who use variance swaps to hedge tail risk. When equity values fall sharply and volatility increases dramatically, decreases in portfolio value are offset by profits on a variance swap that increase at an accelerating rate.