Domestic currency or home currency is the currency of the investor (or the currency in which portfolio results are reported and analyzed).

Domestic asset is an asset denominated in the investor’s domestic currency.

Foreign currency and foreign asset are a currency other that the investor’s domestic currency and an asset denominated in that foreign currency. These are sometimes called the local currency and local market, respectively.

Foreign-currency return (RFC) is the return of the foreign asset measured in its local (foreign) currency. It can be called the local market return.

The percentage change in value of the foreign currency is denoted as RFX. It can be called the local currency return.

Domestic-currency return (RDC) is the return in domestic currency units considering both the foreign-currency return (RFC) and the percentage change in value of the foreign currency (RFX).

Return Decomposition

The domestic-currency return is multiplicative with respect to these two factors:

- RDC = (1 + RFC)(1 + RFX) – 1

where:

RDC is the domestic-currency return (in percent)

RFC is the foreign-currency return

RFX is the percentage change of the foreign currency against the domestic currency.

There are three ways to calculate RDC:

- RDC ≈ RFC + RFX: This approach is an approximation of the more accurate compounded calculation. It emphasizes the two sources of return, RFC and RFX. It is acceptable when precision is not needed, such as selecting between three quite different multiple choice answers or discussing the theoretical sources of return.

- RDC = (1 + RFC)(1 + RFX) – 1 = RFC + RFX + (RFC)(RFX): This approach is precise if the precise RFX is known. I would generally use this approach, unless given clear reasons to do something else.

- However, there are cases where determining RFX is not simple. If the currency is hedged, then a precise currency hedge must short the ending number of foreign currency units; however, that ending number is not knowable for a risky asset. You will see a naïve hedge is normally used and the beginning number of foreign currency units are sold forward. In that case, a simple comparison of Fo and So will not be the true RFX. In that case, you will see a different set of calculations made. You would directly calculate beginning and ending value of the portfolio in the investor’s domestic currency units. Then RDC is (EV – BV) / BV.

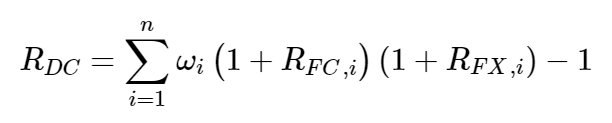

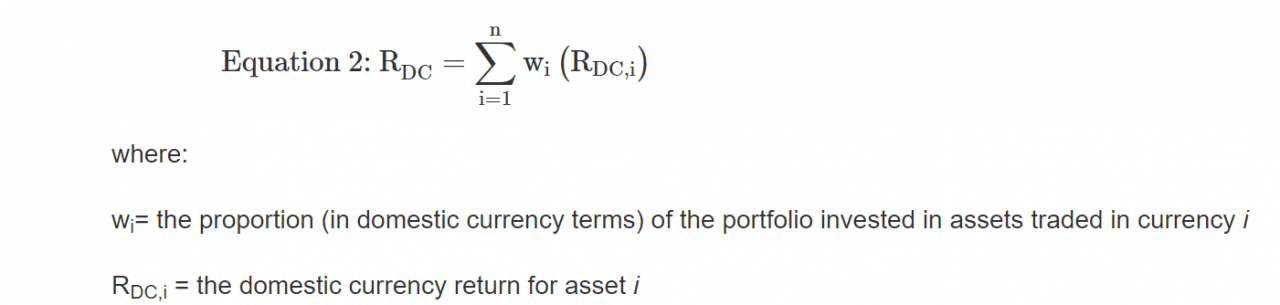

What holds for the domestic-currency return of a single foreign asset also holds for the returns on a multi-currency portfolio of foreign assets, except now the portfolio weights must be considered. More generally, the domestic-currency return on a portfolio of multiple foreign assets will be equal to:

where:

RFC,i is the foreign-currency return on the i-th foreign asset

RFX,i is the appreciation of the i-th foreign currency against the domestic currency

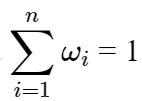

ωi are the portfolio weights of the foreign-currency assets (defined as the percentage of the aggregate domestic-currency value of the portfolio)

Alternatively:

Volatility Decomposition

Now we will turn to examining the effect of currency movements on the volatility of domestic-currency returns. Start by rearranging the equation above:

- RDC = (1 + RFC)(1 + RFX) – 1 = RFC + RFX + RFCRFX

When RFC and RFX are small, then the cross-term (RFCRFX) is small, and as a result this equation can be approximated as:

- RDC ≈ RFC + RFX

We can combine the that with the statistical rule that:

where

X and Y are random variables

ω are weights attached to X and Y

σ2 is variance of a random variable

σ is the corresponding standard deviation

ρ represents the correlation between two random variables

Applying this result to the domestic-currency return approximation leads to:

- σ2(RDC) ≈ σ2(RFC) + σ2(RFX) + 2σ(RFC)σ(RFX)ρ(RFC,RFX)

This equation is for the variance of the domestic-currency returns (RDC), but risk is more typically defined in terms of standard deviation because mean and standard deviation are measured in the same units (percent, in this case).

Hence, the total risk for domestic-currency returns—that is, σ(RDC)—is the square root of the results calculated above.

Examining the equation indicates risk to our domestic investor:

- Depends on the standard deviation of RFC and RFX.

- May be higher for our domestic investor because standard deviation of RFX is an additive term in the equation.

- However, correlation also matters. If the correlation between RFC and RFX is negative, the third component of the calculation becomes negative. The correlation measures the interaction of RFC and RFX.

- If the correlation is positive, then RFC returns are amplified by RFX returns, increasing the volatility of return to our domestic investor.

- If the correlation is negative, then RFC returns are dampened by RFX returns, decreasing the volatility of return to our domestic investor. (This is discussed further under this reading’s topic of minimum variance hedge ratio).

If RFC is a Risk-Free Return: In this case, its standard deviation and correlation with RFX are zero. When RFX is the only source of risk for the domestic investor in the foreign asset, a direct and precise calculation of the standard deviation of RDC is practical.

- Equation 4: σ(RDC) = σ(RFX)(1 + RFC)

where:

RFC = the return on a foreign currency denominated risk-free asset