Investment Philosophy

The entire investment process should be driven by a succinct and precise investment philosophy.

Some managers believe that markets are very efficient and that active management will underperform after considering all related costs. Therefore, those managers will execute passive strategies and attempt to earn risk premiums instead. To earn risk premiums, passive strategies will target one or more specific systematic risk factors including equity risk, credit risk, liquidity risk, and volatility risk.

In contrast, active strategies take the position that markets are inefficient and can allow for those inefficiencies to be exploited when market prices of securities deviate from their intrinsic values.

There are two broad types of inefficiencies to be considered: behavioral and structural. Behavioral inefficiencies are mispricings caused by other investors and their behavioral biases. The mispricings are very short-term in nature and therefore, must be quickly exploited prior to the market correction. Structural inefficiencies occur because of laws and regulations, which can make them long-term in nature.

Whatever the investment philosophy, it is necessary for the manager to be able to convey the underlying assumptions in a clear manner.

- Can the manager clearly and consistently articulate their investment philosophy?

- Are the assumptions credible and consistent?

- How has the philosophy developed over time?

- Are the return sources linked to credible and consistent inefficiencies?

Assuming there is a valid inefficiency to exploit, there is the related issue of capacity.

- Does the inefficiency provide a sufficient frequency of opportunity and level of return to cover transaction costs and fees? If so, does this require leverage?

- Does the inefficiency provide a repeatable source of return? That is, can the opportunity be captured by a repeatable process, or is each opportunity unique, requiring a different process of skill set to exploit?

- Is the inefficiency sustainable? That is, at what asset level would the realized return from the inefficiency be unacceptably low?

Investment Personnel

An investment process can only be as good as the people who create and implement it, and even the best process can be compromised by poor execution by the people involved. This view is not a question of liking the manager or team but of trusting that they possess the expertise and experience to effectively implement the strategy.

- Does the investment team have sufficient expertise and experience to effectively execute the investment process?

- Does the investment team have sufficient depth to effectively execute the investment process?

- What is the level of key person risk?

- What kinds of agreements (e.g., non-compete) and incentives (ownership, bonus, pay) exist to retain and attract key employees to join and stay at the firm?

- What has been the turnover of firm personnel? High personnel turnover risks the loss of institutional knowledge and experience within the team.

Investment Decision-Making Process

The investment decision-making process has four elements: signal creation, signal capture, portfolio construction, and portfolio monitoring.

An investment signal may be a piece of information that can be used to establishing an investment position to exploit an inefficiency.

The efficient market hypothesis posits that the key to exploiting inefficiencies is to have information that is all of the following:

- Unique: Does the strategy rely on unique information? If so, how is this information collected, and how is the manager able to retain an informational edge, particularly in a regulatory environment that seeks to reduce informational symmetries?

- Timely: Does the strategy possess an information timing advantage? If so, how is this information collected, and how is the manager able to retain a timing edge, particularly in a regulatory environment that seeks to reduce informational symmetries?

- Interpreted differently: Interpretation is typically how managers seek to differentiate themselves. Does the manager possess a unique way of interpreting information?

In idea implementation, the investment idea is transformed into an investment position (i.e., signal capture).

- What is the process for translating investment ideas into investment positions?

- Is this process repeatable and consistent with the strategy assumptions?

- What is the process, and who is ultimately responsible for approving an investment position?

The third element is portfolio construction; how investment positions are implemented within the portfolio. This element begins to capture the manager’s risk management methodology. Good investment ideas need to be implemented properly to exploit opportunities and capture desired risk premiums. It is also important that portfolio construction is consistent with the investment philosophy and process as well as the expertise of the investment personnel.

The portfolio allocations may be done quantitatively or qualitatively. Either way, the allocations must make sense in view of the investment philosophy. For example, a passively managed portfolio should not have excessive turnover. The allocations should also account for the manager’s views, therefore, performance maximization would occur by overweighting the expected outperformers and underweighting the expected underperformers. A related issue is the allocation of long and short positions—they may be paired or determined separately. If they are paired, then proper position sizing will eliminate market risk. At the same time, it will allow for the exploitation of inefficiencies prior to the convergence of market prices with intrinsic values.

Assets under management (AUM) will likely increase over time, therefore, the underlying positions may need to be adjusted (e.g., liquidity constraints) to allow for greater AUM.

Stop losses are orders to sell a security once it reaches a certain price and can be an important risk management tool. Hard or soft stop losses may be used. The former involve automatic dispositions when a specific loss threshold is met and the latter involve subjective evaluations when a specified loss threshold is met. As well, hedges are used to manage risk so information about how they are implemented, the financial instruments used to hedge, and the determination of hedge ratios, is necessary.

With liquidity, it should be determined whether the manager is a net supplier or demander of liquidity. Either way, care must be taken to ensure that the portfolio can react appropriately to changing market conditions or investor liquidity requirements. A portfolio that has too many illiquid securities may be faced with high exit costs in addition to the usual high transaction costs. There is also the risk of having to sell securities at depressed prices if funds are suddenly required by the investor. Therefore, in assessing liquidity, there should be an analysis of how much of the portfolio can be liquidated in five days or less (more liquid and therefore, greater flexibility) and well as how much needs more than 10 days to liquidate (less liquid and therefore, subject to higher transaction costs). A calculation of average daily volume (weighted by portfolio position size) is also necessary. Finally, there should be the determination of any security where the firm owns more than 5% of its total market capitalization as that would suggest some liquidity problems if the entire position needed to be disposed of suddenly.

The monitoring process looks at external factors such as the general economy and financial markets and their impact on how the manager may exploit relevant inefficiencies. It also looks at internal factors such as historical returns, risk level, and allocations. There is a check for any significant deviations from the investment process (e.g., style drift) and to ensure that investment decisions are congruent with the most up-to-date client objectives.

Operational Due Diligence

Regardless of the strength of the investment process or the historical investment results, investment management firms must be operated as a successful business in order to ensure their sustainability.

This requirement creates the potential for a misalignment of interests between the manager and the investor. Operational due diligence analyzes the integrity of the business and seeks to understand and evaluate these risks by examining and evaluating the firm’s policies and procedures.

Weaknesses in the firm’s infrastructure represent latent risks to the investor. A strong back office is critical for safeguarding assets and ensuring that accurate reports are issued in a timely manner. The allocator needs to understand the following:

- What is the firm’s trading policy?

- Does the firm use soft dollar commissions? If so, is there a rigorous process for ensuring compliance?

- What is the process for protecting against unauthorized trading?

- How are fees calculated and collected?

- How are securities allocated across investor accounts, including both pooled and separately managed accounts? The allocation method should be objective (e.g., based on invested capital) to avoid the potential to benefit some investors at the expense of others.

- How many different strategies does the firm manage, and are any new strategies being contemplated? Is the firm’s infrastructure capable of efficiently and accurately implementing the different strategies?

- What information technology offsite backup facilities are in place?

- Does the firm have processes, software, and hardware in place to handle cybersecurity issues?

An important constituent of the infrastructure is third-party service providers, including the firm’s prime broker, administrator, auditor, and legal counsel. They provide an important independent verification of the firm’s performance and reporting.

- Are the firm’s third-party service providers known and respected?

- Has there been any change in third-party providers? If so, when and why? This information is particularly important with regard to the firm’s auditor. Frequent changes of the auditor is a red flag and may mean the manager is trying to hide something.

The risk management function should be viewed as an integral part of the investment firm and not considered a peripheral function. The extent to which integration exists provides insight into the firm’s culture and the alignment of interests between the manager and the investor. The manager should have a risk manual that is readily available for review:

- Does the portfolio have any hard/soft investment guidelines?

- How are these guidelines monitored?

- What is the procedure for curing breaches?

- Who is responsible for risk management?

- Is there an independent risk officer?

An investment management firm must operate as a successful business to ensure sustainability. A manager that goes out of business does not have a repeatable investment process. An important aspect of manager selection is assessing the level of business risk.

- What is the ownership structure of the firm?

- What are the total firm AUM and AUM by investment strategy?

- What is the firm’s breakeven AUM (the asset base needed to generate enough fee revenue to cover total firm expenses)?

- Are any of the firm’s strategies closed to new capital?

- How much capital would the firm like to raise?

A firm that is independently owned may have greater autonomy and flexibility than a firm owned by a larger organization, but it may have a higher cost structure and lack financial support during market events, raising potential business risks. Outside ownership could create a situation in which the outside owner has objectives that conflict with the investment strategy. Ideally, ownership should be spread across as many employees as is feasible and practical.

A firm managing a smaller asset base may be more nimble and less prone to dilution of returns but will likely have lower revenues to support infrastructure and compensate employees. At a minimum, the asset base needs to be sufficient to support the firm’s current expenditures.

Last are legal and compliance issues. It is critical that the firm’s interests are aligned with those of the investor.

- What are the compensation arrangements for key employees?

- Do employees invest personal assets in the firm’s strategies?

- Does the firm foster a culture of compliance?

- What is covered in the compliance manual?

- Has the firm or any of its employees been involved with an investigation by any financial market regulator or self-regulatory organization?

- Has the firm been involved in any lawsuits?

- Are any of the firm’s employees involved in legal actions or personal litigation that might affect their ability to continue to fulfill their fiduciary responsibilities?

There are two broad options for implementing investment strategies: individual separate accounts and pooled (or commingled) vehicles. An additional operational consideration is the evaluation of the investment vehicle—its appropriateness to the investment strategy and its suitability for the investor. Separate accounts offer additional control, customization, tax efficiency, reporting, and transparency advantages, but these come at a higher cost.

Separately managed accounts (SMAs) and pooled investment vehicles are used to execute investment strategies. Pooled vehicles bring together the funds from all investors into one portfolio and there is no customization for any specific investor. SMAs hold the funds of one investor in a separate account so a key analysis is the cost-benefit trade-off of holding investments in a SMA. As well, one must ensure the manager has the capability and resources to manage the SMA.

Compared to pooled investments, SMAs have higher transaction costs but provide control, customization, tax efficiency, separate reporting, and greater transparency.

- Ownership: In an SMA, the investor owns the individual securities directly. This approach provides additional safety should a liquidity event occur. Although the manager continues to make investment decisions, these decisions will not be influenced by the redemption or liquidity demand of other investors in the strategy. An SMA also provides clear legal ownership for the recovery of assets resulting from unforeseen events, such as bankruptcy or mismanagement.

- Customization: SMAs allow the investor to potentially express individual constraints or preferences within the portfolio. SMAs can thus more closely address the investor’s particular investment objectives.

- Tax efficiency: SMAs offer potentially improved tax efficiency because the investor pays taxes only on the capital gains realized and allows the implementation of tax-efficient investing and trading strategies.

- Transparency: SMAs offer real-time, position-level detail to the investor, providing complete transparency and accurate attribution to the investor. Even if a pooled vehicle provides position-level detail, such information will likely be presented with a delay.

Customized SMAs require an extra layer of due diligence to evaluate security selection, portfolio construction, and operational issues. Cost-wise, SMAs have fixed costs that must be borne entirely by the one investor and cannot be spread amongst multiple investors in the case of pooled investments.

For pooled investments, the incremental costs of adding additional investors are relatively low whereas SMAs require a separate account for each investor. Trading costs are relatively higher for SMAs because trades cannot be aggregated to reduce trading volumes. A customized SMA will differ from the benchmark so it creates tracking risk due to investor constraints instead of manager actions. Customized SMAs are subject to micromanagement risk on the part of the investor and that makes it difficult to determine the true value added by the manager . Investors may be subject to trend chasing, avoidance of unfamiliar investments, and not understanding the benefits of hedging.

An additional and important aspect of manager selection is understanding the terms of the investment as presented in the prospectus, private placement memorandum, and/or limited partnership agreement.

Closed-end funds and ETFs have the highest liquidity because they are traded intra-day. Open-end funds offer almost as much liquidity in that they are traded based on end-of-day NAV only.

Investments held in limited partnership structures (e.g., hedge funds, private equity, and venture capital) usually involve investment capital that is tied up for more time.The lockup period refers to the period immediately following the initial investment, where funds may not be withdrawn. A hard lock does not permit redemptions, while a soft lock permits redemptions for a fee. Gates provide for a limit in the redemption amount for any given redemption.

Private equity and venture capital funds have the lowest liquidity because of capital calls; investors only receive returns after about five years into the 10-year average life of the funds. The manager may extend the life of the fund for up to two one-year periods, which further lowers liquidity.

Key advantages of limited partnership terms include ability to have a long investment horizon, thereby not allowing investors to overreact to short-term aberrations. As well, allowing for the earning of illiquidity premiums by investing in illiquid assets and not being forced to sell assets at depressed prices due to redemption requests.

Key disadvantages of limited partnership terms include the impaired ability to change portfolio allocations in response to changes in the market. As well, the impaired ability to meet sudden liquidity demands.

With SMAs, the liquidity is determined by the liquidity of the underlying assets, as the securities can be sold at any time

Managers charge fees to cover their fixed and variable costs as well as to earn a profit. The average asset-weighted expense ratio paid by mutual investors has declined substantially over the years as investors have increasingly allocated to no-load mutual funds and index funds which have lower fees.

Mutual fund fees are often based on AUM. In some cases, minimum balances are required. Fees can be structured as a fixed dollar amount or on the basis of a percentage of assets. The fee structure is important to ensure that managers work to the advantage of the investors.

An advantage of the investor paying fees based on AUM is that it rewards based on the manager’s skill and ability to grow the asset base.

Performance-based fees are a form of risk sharing between the investor and the manager in order to align their interests. They are computed on the basis of total or relative return. The fees (using a sharing percentage) could be based on total performance or performance in excess of a base.

There are three basic forms of performance-based fees:

- Symmetrical structure with full upside and downside exposures.

- Fee = base + performance sharing

- The greatest alignment between investor and manager incentives but increased risk to manager due to the full downside exposure

- Bonus with full upside and limited downside exposures.

- Fee = Greater of: (1) base, (2) base + sharing of positive performance

- Bonus with limited upside and downside exposures.

- Fee = Greater of: (1) base, (2) base + sharing of positive performance (within limit)

Performance-based fee structures transform symmetrical gross active return distributions into asymmetrical net active return distributions. The result is lower relative variance on the upside versus the downside. Therefore, by using a symmetrical risk measure such as standard deviation, there could be an underestimation of downside risk.

Performance-based fees benefit investors since they will pay relatively lower performance-based fees in the case of low active returns. Such fees benefit managers, as they may incentivize them to increase their efforts to benefit the investor’s portfolio and to increase their own compensation. However, all three structures have in common the fact that base fees are paid even when the manager underperforms.

Some investments have no limits on performance fees. In some cases, performance fees could be tempered to include high-water or clawback provisions that will offset prior period negative returns from current period positive returns, for example. For private equity partnerships, the investors are structured as limited partners and the manager as the general partner. A beneficial term for the investors is one that stipulates the repayment of principal and share of profits to the limited partners prior to any payment of performance fees to the general partner.

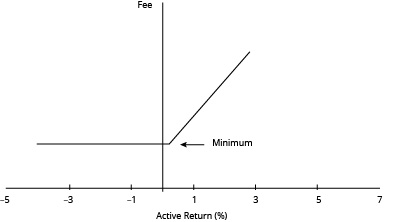

This bonus fee structures are analogous to a manager having a long position in a call option on the portfolio active return. The exercise price would be the base fee. See Payoff Line of Sample Performance-Based Fee Schedule 1 for a graphical representation. The payoff to the manager is theoretically unlimited.

Payoff Line of Sample Performance-Based Fee Schedule 1

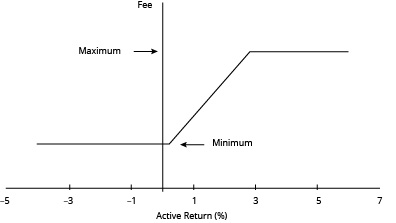

In Payoff Line of Sample Performance-Based Fee Schedule 2, there is the addition of a short position in a less valuable call option with an exercise price equal to the maximum fee).

Payoff Line of Sample Performance-Based Fee Schedule 2

Based on the this discussion, a net long position in a call option on portfolio active return, would cause a manager to take more risk since option pricing theory states that higher volatility increases option value. Therefore, it is recommended that managers be both penalized for taking too much risk and rewarded for earning higher risk-adjusted returns.