Purchasing insurance trades a reduction in expected lifetime consumption for an increase in the stability of expected spending after a loss.

Life insurance provides a hedge against the risk of the premature death of an earner.

Life insurance can also be an important estate-planning tool. A life insurance policy can provide immediate liquidity to a beneficiary without the delay involved in the legal process of settling an estate following the death of an individual.

Another possible use of life insurance is as a tax-sheltered savings instrument, notably in the United States. As mentioned previously in this reading, cash-value policies invest a portion of the premium in a tax-advantaged account that represents the difference between the current cost of providing insurance coverage and the premium.

The mortality charge is the cost of providing life insurance, which increases with age. As mortality risk increases, the accumulated excess premium can be used to pay the increasingly higher costs of providing insurance protection. These excess premiums can be invested in a variety of instruments that can grow over time sheltered from taxation and can eventually be cashed out without paying for older-age life insurance protection.

Life insurance protects human capital, which is defined as the present value of future labor

income. Information that affects human capital: (1) salary level and (2) correlation between wage

growth and risky-asset returns. Higher salary (wages) implies higher future wages and thus

higher human capital. Higher correlation implies more volatile (riskier) wages; using a higher

discount rate to account for results in a lower value for human capital. The case also provides

asset levels for Debra and Kelly. All else constant, financial wealth is a substitute for life

insurance. The higher the financial wealth, the lower the demand for insurance.

Basic Life Insurance Terminology

Life Insurance protects against the loss of human capital for those who depend on an individual’s future earnings.

- Benefits or face amount. The future payout. The terms may specify payout as a lump sum or an annuity.

- Premium. The cost of the insurance.

- Cash value. What the owner can withdraw before payout, which reduces or terminates final payout.

- Paid up. A date when the insurance is fully paid for and no additional premiums are required.

- Limitations. Restrictions on the payout of the insurance amount (e.g., misrepresentation of the health status of the insured leading to no payment).

- Contestability period. Time period for the insurance company to investigate or deny payment of the claim.

- Identity of the insured.

- Policy owner. Responsible for making premium payments, often the insured. If the owner is not the insured, he must have an insurable interest in the insured. In other words, the owner must have a vested interest in the continued life of the insured and not simply be speculating on the insured’s death.

- Beneficiaries. Receivers of the payout.

- Premium schedule. Amount and frequency of payments.

- Riders. Additional provisions included in the policy.

- Modifications. Allowable changes that can be made to the policy.

Types of Life Insurance

Life insurance protects the survivors from the adverse financial consequences of the insured’s premature death. The optimal amount of insurance depends on the cost of the insurance and the loss in value to the survivors caused by the death. The insurance can also provide liquidity to meet death and estate expenses. This is more important if the other estate assets are illiquid. Some life insurance provides tax benefits by accumulating cash value on a tax-sheltered basis.

- Temporary (term) insurance covers only a designated period such as 1, 5, or 20 years. The cost can be fixed or increasing over the designated period. The policy then ceases at the end of the period unless it includes a provision to renew the policy. Term insurance is less costly than permanent insurance because the mortality risk is lower for the insurance company as the individual’s risk of dying increases later in life (after the insurance ceases). The mortality risk also means term insurance for younger individuals and for shorter time periods will cost less than for older individuals and longer periods, all other factors the same.

- Permanent insurance is more costly and lasts for the life of the insured. The premium (cost) per period is usually fixed, and the policy builds value as the premium exceeds the pure cost of insurance in the initial years. In later years, this built up value covers the increasing cost that would be paid for pure (term) insurance. Permanent insurance can be categorized as whole life or universal insurance.

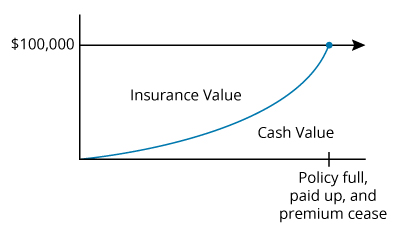

Insurance Versus Cash Value in Permanent Insurance for $100,000

Whole life typically has a fixed annual premium payment. The policy continues and the policy cannot be canceled by the insurance company as long as premiums are paid. The non-cancelability makes purchase at a young age more desirable as new insurance may be unavailable or much more expensive if the insured person’s health deteriorates. The policy may also reach a fully paid status in later years and require no further premiums. Participating whole life shares in company profits and may increase in value more quickly.

Universal life is similar in concept but with more flexibility. The premium payment can be increased or decreased to increase or decrease the amount of insurance and/or the rate at which cash value grows. There may be investment choices for where the premiums are invested. Premium payments can be discontinued and the insurance continues (a non-forfeiture clause) as long as the cash value and earnings on the cash value are sufficient to pay the pure (term) cost of insurance each period.

Life insurance policies can include riders, which provide additional benefits.

Basic Elements of a Life Insurance Policy

Life insurance pricing is simple in concept but complex in application. It is a large time value of money problem. The insurance company must charge sufficient premiums such that the money after investing the premiums is sufficient to pay the policy benefits, cover the company’s costs, and leave a profit. The company is applying the law of large numbers. The remaining term of life for any one individual is highly uncertain, but predictable in aggregate for a large group. The pricing model can be broken down into three issues:

- Mortality estimates. Mortality tables are built to reflect past experience and future projections of mortality. Probability of death (1 − probability of life) can be refined and based on age, health, gender, and lifestyle choices. The insurance company will gather information regarding the insurability of the applicant and may employ third party investigators and medical professionals to assess the risk factors. The company’s goal is to avoid adverse selection and undercharging for the risks assumed.

- Net premium. Based on the assumed mortality rates, the company estimates the net premiums to charge for insurance based on an assumed discount rate. The discount rate is also the assumed rate of return on investing the premiums. At that discount rate, the premiums must be sufficient such that the PV of the premiums and payouts are equal.

- Load. The load plus net premium is the gross premium charged for the insurance. The load must cover the company’s operating cost and expenses for writing the policy. This can include a sales commission to sell the policy and cost of any medical tests to determine insurability

For a simple one-year term insurance policy, the application is relatively simple. Risk is limited as only one year of variables must be considered to estimate the net premium for pure insurance. Load will also be fairly simple to estimate. If the policy is renewed the following year, a new gross premium will be calculated. For a level payment multi-year term policy, the process is slightly more complex. The level premium will be higher than the year 1 and less than the year 5 premium for annual term. The premium is conceptually a weighted average of five sequential one-year term premiums. In reality, it should be higher as the company is at greater risk; it must project the relevant variables for the five-year period and cannot change the premium each year.

Permanent insurance pricing extends the same concepts, but with more uncertainty as the ultimate life expectancy of the insured individual has to be considered. The longer time period puts the insurance company at greater risk in correctly estimating mortality rate, discount rate (return on invested premiums), and expenses. These factors will make the initial premium higher. In addition, many such policies include a buildup of cash value that the policyholder can access before policy payout. The cash buildup is created by charging an even higher premium. Such policies typically include a paid up date when return on cash value is sufficient to pay future costs of insurance and premiums cease.

Comparing cost between insurance policies becomes more difficult as policy complexity increases. For annual term, when all else is the same, the lowest premium is lowest cost. For permanent insurance, the number of variables makes comparison complex as it is highly unlikely any two policies will be the same. Two common approaches are the net payment cost index and net surrender cost index. Both require an assumed age of death for the insured and a discount rate. The second also requires a cash value projection.

Other Types of Insurance

- Disability income insurance provides partial replacement of the insured’s job income if the job is lost.

- Property insurance provides compensation for losses in value of real property. Homeowners insurance covers the home, and automobile insurance covers the car.

- Health and medical insurance covers health care expense.

- Liability insurance covers losses if the insured is found legally responsible for damages to another.