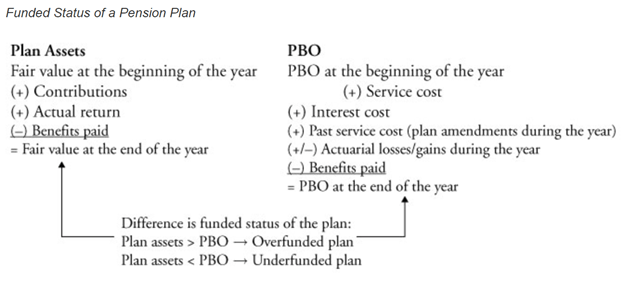

The projected benefit obligation (PBO) [known as present value of defined benefit obligation (PVDBO) under IFRS] is the actuarial present value (at an assumed discount rate) of all future pension benefits earned to date, based on expected future salary increases.

From one period to the next, the benefit obligation changes as a result of current service cost, interest cost, past (prior) service cost, changes in actuarial assumptions, and benefits paid to employees.

Current service cost is the present value of benefits earned by the employees during the current period. Service cost includes an estimate of compensation growth (future salary increases) if the pension benefits are based on future compensation.

Interest cost is the increase in the obligation due to the passage of time. Benefit obligations are discounted obligations; thus, interest accrues on the obligation each period. Interest cost is equal to the pension obligation at the beginning of the period multiplied by the discount rate.

Changes in actuarial assumptions are the gains and losses that result from changes in variables such as mortality, employee turnover, retirement age, and the discount rate. An actuarial gain will decrease the benefit obligation and an actuarial loss will increase the obligation.

Benefits paid reduce the PBO.

The total periodic cost, also known of periodic pension cost or net periodic pension cost, is the employer contribution for a period adjusted for the funded status. If the funded status is positive, the pension expense for the company is considered paid, other wise the expense is considered deferred, leading to an increase in cost above what the employer normally owes.

total periodic pension cost (TPPC) = employer contributions − (ending funded status − beginning funded status)

This is the change in funded status from the two periods we are comparing.

We can also rewrite this equation as:

total periodic pension cost = current service cost + interest cost − actual return on plan assets +/– actuarial losses/gains due to changes in assumptions affecting PBO + prior service cost

Current service cost. Current service cost is the present value of benefits earned by the employees during the current period. Current service cost is immediately recognized in the income statement.

Interest cost. Interest cost is the increase in the PBO due to the passage of time. It is calculated by multiplying the PBO at the beginning of the period by the discount rate. Interest cost is immediately recognized as a component of pension expense.

Under IFRS, net interest expense/income is defined as the discount rate multiplied by the beginning funded status (i.e., interest cost is offset against expected plan return). If the plan is reporting a liability (i.e., an underfunded plan), an expense is reported. Conversely, if the plan reports an asset, interest income is reported.

Expected return on plan assets. However, the expected return on the assets is a component of reported pension expense. Expected return (instead of actual return) on plan assets is used for the computation of reported pension expense. The difference in the expected return and the actual return is combined with other items related to changes in actuarial assumptions into the “actuarial gains and losses” account. Under IFRS, the expected rate of return on plan assets is implicitly assumed to be the same as the discount rate used for computation of PBO and a net interest expense/income is reported as discussed above.

Actuarial gains and losses. The first component is the gain (loss) due to decrease (increase) in PBO occurring on account of changes in actuarial assumptions; the second component is the difference between actual and expected return on plan assets.

Actuarial gains and losses are recognized in other comprehensive income (OCI). Under IFRS, actuarial gains and losses are not amortized. Under U.S. GAAP, actuarial gains and losses are amortized using the corridor approach.

Difference Between Recognition of Components of Pension Costs Under U.S. GAAP and IFRS

| Component | U.S. GAAP | IFRS |

| Current service cost | Income statement | Income statement |

| Past service cost | OCI, amortized over service life | Income statement |

| Interest cost | Income statement | Income statement |

| Expected return | Income statement | Income statement* |

| Actuarial gains/losses | Amortized portion in income statement. Unamortized in OCI. | All in OCI—not amortized (called ‘Remeasurements’) |

| *Under IFRS, the expected rate of return on plan assets equals the discount rate and net interest expense/income is reported. |

Other Equations for Benefit Plan Calculations:

The funded status reflects the economic standing of a pension plan:

funded status = fair value of plan assets − PBO

The balance sheet presentation under both U.S. GAAP and IFRS is as follows:

balance sheet asset (liability) = funded status

If the funded status is negative, it is reported as a liability. If the funded status is positive, it is reported as an asset.

End of year PBO = Beginning of year PBO + current service costs + interest cost + past service costs + actuarial gain/loss – benefits paid

End of year Plan Assets = BOY Plan Assets + employer contributions + actual return + benefits paid

Beginning funded status = beginning plan assets – beginning PBO

Ending funded status = ending plan assets – ending PBO

Periodic Pension Cost in P&L = Current service cost + interest cost – expected return on plan assets

Periodic Pension Cost in P&L IFRS = Current service cost + past service cost (total) + net interest cost

Periodic Pension Cost in OCI = total periodic pension cost – periodic pension cost in P&L