Market participants prefer the swap rate curve as a benchmark interest rate curve rather than a government bond yield curve for the following reasons:

- Swap rates reflect the credit risk of commercial banks rather than the credit risk of governments.

- The swap market is not regulated by any government, which makes swap rates in different countries more comparable. (Government bond yield curves additionally reflect sovereign risk unique to each country.)

- The swap curve typically has yield quotes at many maturities, while the U.S. government bond yield curve has on-the-run issues trading at only a small number of maturities.

Wholesale banks that manage interest rate risk with swap contracts are more likely to use swap curves to value their assets and liabilities. Retail banks, on the other hand, are more likely to use a government bond yield curve.

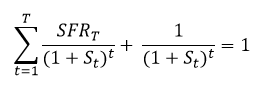

In the equation below, SFR can be thought of as the coupon rate of a $1 par value bond given the underlying spot rate curve.