We can value a put option using put call parity. Put-call parity states that the value of a fiduciary call is equal to the value of a protective put. A fiduciary call is a long call plus an investment in a zero coupon bond whose face value is equal to the call’s strike price. A protective put is being long a stock and long a put. The two options in the relationship should have the same maturity and exercise price.

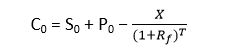

S0 + P0 = C0 + PV(X)

Recognizing this relationship, we can use it to create synthetic instruments. For instance, we can create a synthetic call by combining a long stock position, a long put, and shorting a zero-coupon bond.

C0 = S0 + P0 − PV(X) or