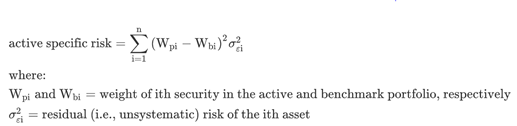

In a multifactor model, active risk can be broken down into two parts, active factor risk and active specific risk. Active factor risk is risk caused factor tilts in a portfolio that deviate from the benchmark’s sensitivities from the same factors, while active specific risk comes from deviations in the portfolios individual asset weightings compared to the benchmark.

The active risk squares is the sum of the active factor risk and the active specific risk.

active risk squared = active factor risk + active specific risk

Active factor risk represents the risk explained by deviation of the portfolio’s factor exposures relative to the benchmark and is computed as the residual (plug):

active factor risk = active risk squared – active specific risk