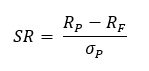

For review, the Sharpe ratio (SR) is the excess return per unit of risk. It is unaffected by cash inflows or leverage. By adding a 50% position in a risk-free asset would reduce the excess return and standard deviation by half.

The Sharpe ratio is shown below:

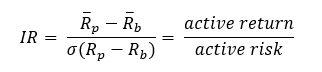

The information ratio is active return over active risk, which is the standard deviation of active returns:

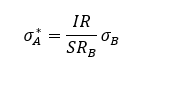

The optimal amount of risk for an active unconstrained portfolio is the amount of risk that maximizes the Sharpe ratio, calculated by the eqn:

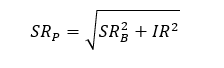

The Sharpe ratio of a portfolio with optimal level of active risk can be calculated as:

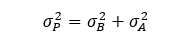

Furthermore, the total risk of the portfolio is given by:

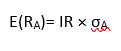

The expected active return given an active risk:

Portfolio P’s excess return =

A few key concepts to note:

- A closet index fund is a fund that is purported to be actively managed but in reality closely tracks the underlying benchmark index. These funds will have a Sharpe ratio similar to that of the benchmark index, a very low information ratio, and little active risk. After fees, the information ratio of a closet index fund is often negative.

- A fund with zero systematic risk (e.g., a market-neutral long-short equity fund) that uses the risk-free rate as its benchmark would have an information ratio that is equal to its Sharpe ratio. This is because active return will be equal to the portfolio’s return minus the risk-free rate, and active risk will be equal to total risk.

- Unlike the Sharpe ratio, the information ratio will change with the addition of cash or the use of leverage.

- The information ratio of an unconstrained portfolio is unaffected by the aggressiveness of the active weights. If the active weights of a portfolio are tripled, the active return and the active risk both triple, leaving the information ratio unchanged.

- If we combine an actively managed portfolio with an allocation to the benchmark portfolio, the resulting blended portfolio will have the same information ratio as the original actively managed portfolio. As we increase the weight of the benchmark portfolio, the active return and active risk decrease proportionately, leaving the information ratio unchanged.

- Investors can select an appropriate amount of active risk by investing a portion of their assets in the active portfolio and the remaining portion in the benchmark. For example, if the active risk of a fund is 10%, an investor seeking to limit active risk to 6% can do so by investing 60% in the active portfolio and the remaining 40% in the benchmark portfolio.