Lifetime Gifts and Testamentary Bequests

A method of transferring discretionary wealth is to donate it immediately or during one’s lifetime through a series of gratuitous transfers. In jurisdictions having an estate or inheritance tax, gifting has the advantage of lowering the value of the taxable estate, thereby lowering estate or inheritance taxes.

To mitigate this tax minimization strategy, jurisdictions that impose estate or inheritance tax typically also impose gift or donation taxes.

A client with excess capital can gift the capital now or bequest it at death. There are practical issues to consider: Gifting now likely gives up control and cannot be revoked if circumstances change. There are also tax issues to consider that can affect the ultimate value of the gift/bequest to the receiver.

One approach is to calculate a ratio of a gift now versus bequest at death. A ratio above/below 1 indicates that from a tax perspective it is favorable/unfavorable to gift now. The calculations are based on the FV after-tax to the receiver. Any FV after-tax calculations require assumptions and the conclusions are only as good as the assumptions.

The basic form of the ratio is:

There are three tax scenarios to consider:

- The gift now is tax free to both the receiver and the donor.

- The gift now is taxable with the tax paid by the receiver.

- The gift now is taxable with the tax paid by the giver, also called the donor.

The relevant tax factors to consider are:

- rg and tig are the pretax return earned and the applicable tax rate on those earnings for assets held by the gift receiver.

- re and tie are the pretax return earned and the applicable tax rate on those earnings for assets held by the gift giver.

- Te is the estate tax rate and would be paid from the estate.

- Tg is the gift tax rate, paid by the giver (or by the receiver if specified by the facts in the question).

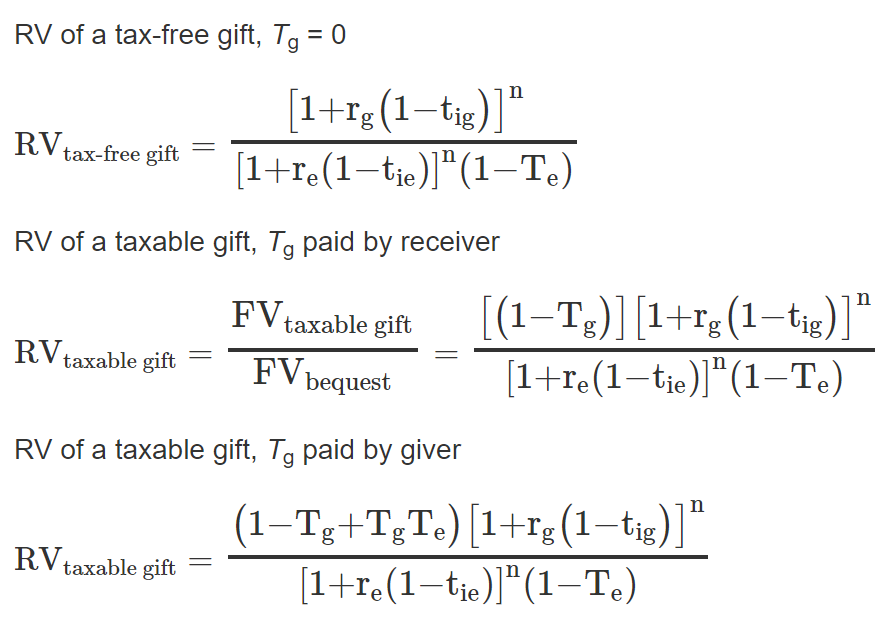

The three potential RV ratios are:

Notice that each formula is a cumulative variation on the previous formula.

RV of a tax-free gift, Tg = 0: The numerator projects FV after-tax of the investment if held by the receiver. The denominator projects the FV after-tax if held by the giver and then subject to estate taxes.

RV of a taxable gift, Tg paid by receiver: This is a variation on the tax-free gift formula with a subtraction in the numerator of −Tg to reflect the receiver of the gift must pay a tax and has less to invest. All else the same, it makes gifting now less attractive.

RV of a taxable gift, Tg paid by giver: This is a variation on the taxable gift if paid by receiver formula with the addition of +TgTe in the numerator. All else the same, the giver’s estate is reduced and therefore the future estate tax will be lower. One interpretation is gifting now creates a partial gift tax credit against the estate tax bill.

Generation Skipping

In the absence of generation-skipping transfer taxes, as in the United States, transferring assets directly to a third generation avoids possible double taxation. When the first generation transfers assets to the second generation, the transfer is typically subject to taxes. Then when the second generation transfers the assets to the third generation, the assets are taxed again.

Spousal Exemptions

Many countries allow tax-free transfers of estates between spouses. Whether or not this is optimal from a tax perspective depends upon other possible gift and inheritance exclusions.

Valuation Discounts

Assets such as marketable securities have readily determined fair market values, but valuing ownership claims in partnerships and other privately held interests can be difficult. Because valuation discounts can reduce the value of wealth transfers and the associated transfer taxes, high net worth individuals will utilize them whenever possible by, for example, transferring interest in a family business.

The value of a nonpublicly traded family business is determined using financial models with discount rates and other assumptions from otherwise comparable publicly traded firms. The resulting value, of course, implicitly assumes the family business is also publicly traded, so the valuator must reduce it to reflect the family business’s lack of liquidity. In addition, the proportion of the family business transferred may not give the recipient control of the firm’s operations, so the value could also be subject to a minority interest discount.

An important consideration is that discounts are not typically additive.

Deemed Dispositions

Rather than impose an estate or inheritance tax on the amount of capital bequeathed at death, some countries treat bequests as deemed dispositions, that is, as if the property were sold. The deemed disposition triggers the realization of any previously unrecognized capital gains and liability for associated capital gains tax. The tax is therefore levied not on the principal value of the transfer, but only on the value of unrecognized gains, if any.

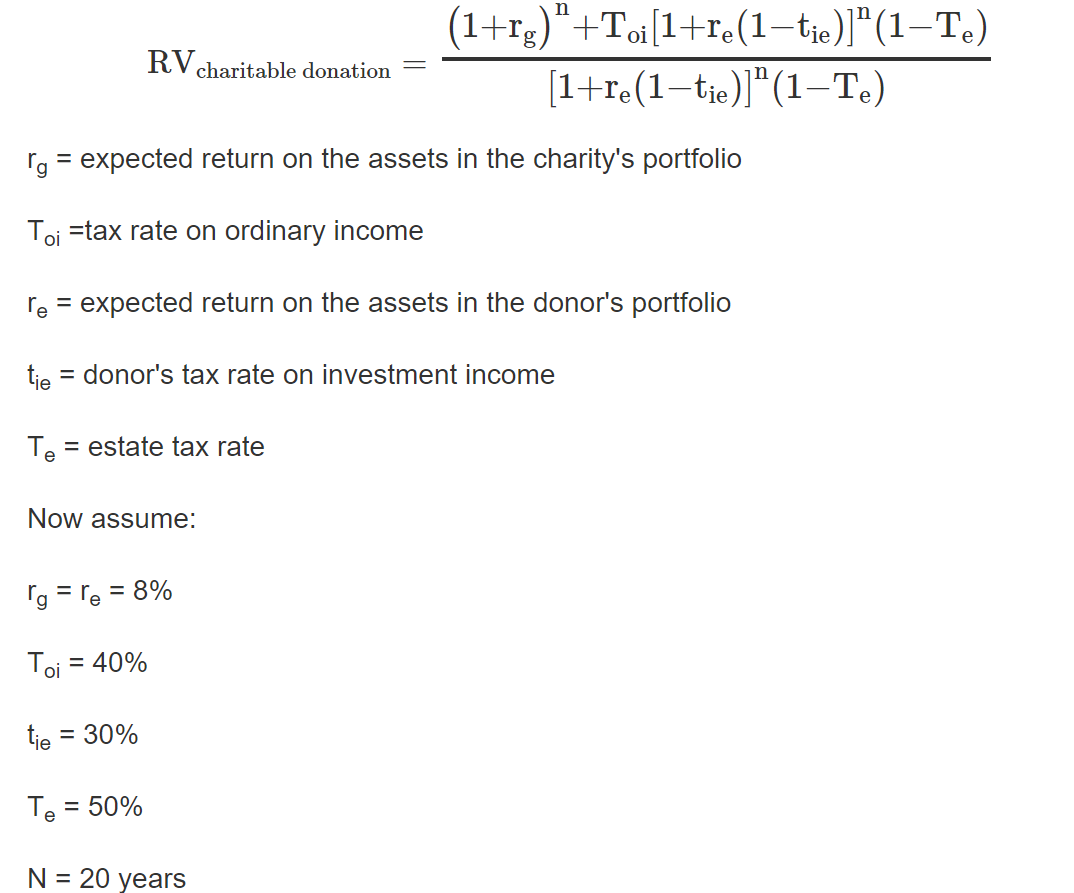

Charitable Gratuitous Transfers

If the gift receiver is a tax-exempt charity, this creates another variation of the RV formulas. The denominator is the same as in the previous equations; the giver invests, an estate tax is paid at death, and then the bequest is made. The numerator, which is the FV to the receiver if gifted now, is different and almost always higher because:

- The charity can invest and the asset return earned is not taxed. This is the (1 + rg)n term.

- The giver can take an immediate tax deduction for the gift and this will reduce the giver’s current tax bill by Toi for each dollar gifted. Toi is the giver’s tax rate on ordinary income. Therefore a $1.00 gift would produce a tax savings of $1.00(Toi). The formula compounds this tax savings to a FV subject to estate taxes and then bequested at death, as an addition to the gift made now. This is the remainder of the formula in the numerator.

RV of a gift to a charity: