Defined-benefit plan

Defined benefit plans are pension plans where the employer promises to make periodic payments to an employee after the employee retires. This involves a more complicated accounting requirement than defined contribution plans for instance, due to the many variables required to ensure that payments are made.

Funded Status

The funded status of the plan is there between the fair value or plan assets and the project benefit obligation.

- Funded Status = Fair Value of Assets – Benefit Obligation

The funded status is part of the balance sheet presentation as an asset or liability under both GAAP and IFRS.

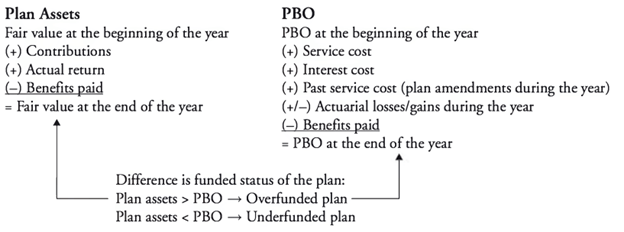

The change in funded status is the difference between start of year funded status and start of year benefit obligation. We can adjust BOY Fair Value and Benefit Obligations to EOY values using the following equations:

- EOY Fair Value = BOY Fair Value + contribution + Actual Return – Benefits Paid

- EOY PBO = BOY PBO + Service Costs + Interest Costs + Past Service Cost +/- Actuarial Gain/Loss – benefits paid

Service cost is the increase in PBO resulting from earned pension benefits during the year.

Under both GAAP and IFRS, all but Past Service Costs and Actuarial Gains/losses are reported on the income statement. Under GAAP Past Service Costs is amortized over the service life in OCI, whereas in IFRS it is treated under Income Statement as an expense. Past service costs are essentially changes in service cost due to plan amendments.

Actuarial gains and loses are all reported in OCI under IFRS as an unamortized remeasurement, but under GAAP, a portion is amortized in the income statement and the rest is reported in OCI. Actuarial gains/loses are cause by changes in actuarial assumptions or differences between the actual and expected return on plan assets.

- Remeasurements = Net return on plan assets = Actual Return – Net interest income/expense

Periodic Pension Costs

The change in funded status can also be found by subtraction the total periodic pension cost from the employer contribution.

- Change in Net Pension Asset or Liability = Employer Contribution -Total Periodic Pension Cost

We can find the periodic pension cost by adjusting the above equation

- Periodic Pension Cost = Employer Contribution – Change in funded status

or by adding the components of periodic pension costs individually.

- Periodic Pension Cost = current service cost + interest cost – actual return +/- actuarial gains/loses + prior service cost

Note that Periodic Pension Cost is different from Pension Expense, which uses expected returns as its basis:

- Pension Expense (IFRS) = service cost + past service cost + net interest expense

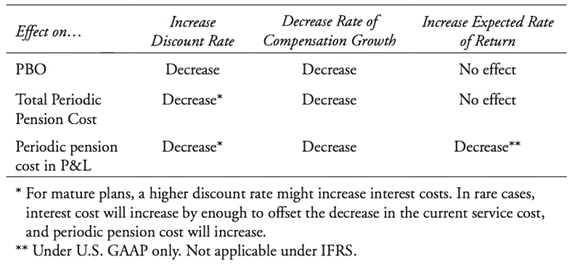

Translating Changes in Assumption to Changes on the Balance Sheet

Firms use three assumptions in pension calculations:

- The discount rate to compute PV of benefit obligations and current service costs is based on the interest rates of high quality fixed income products with maturity profiles close to the benefit obligation

- The rate of compensation growth is the average annual rate by which employee compensation is expected to increase over time

- The expected return on plan assets is the assumed long-term rate of return on the plan’s assets

Changing these slightly can lead to changes in the reporting of the pension plan.

Firms can improve reporting by increasing discount rate, reducing compensation growth rate or increasing the expected return on plan assets.