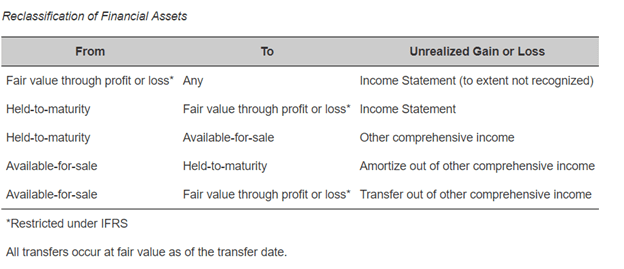

Under IFRS, securities cannot be reclassified in or out of the Fair Value designation, it is considered irrevocable. Reclassification of debt from held-for-trading to FV is permitted under business model changes, but is otherwise restricted under IFRS.

Debt securities classified as available-for-sale can be reclassified as held-to-maturity if the holder intends to (and is able to) hold the debt to its maturity date. Balance sheet is re-measured to reflect new FV, gains and losses and gains from reclassification are amortized in other comprehensive income.

Held-to-maturity securities can be reclassified as available-for-sale if the holder no longer intends or is no longer able to hold the debt to maturity. Carry value is re-measured to fair value, and difference record in other comprehensive income. Reclassifying one security as available from same may prevent a firm from using the Held-to-maturity designation in the future, and may even require conversion of other held-to-maturity securities.

U.S. GAAP does permit securities to be reclassified into or out of held-for-trading or designated at fair value. Unrealized gains are recognized on the income statement at the time the security is reclassified. For investments transferring out of available-for-sale category into held-for-trading category, the cumulative amount of gains and losses previously recorded under other comprehensive income is recognized in income. For a debt security transferring out of the available-for-sale category into the held-to-maturity category, the cumulative amount of gains and losses previously recorded under other comprehensive income is amortized over the remaining life of the security. For transferring investments into the available-for-sale category from the held-to-maturity category, the unrealized gain/loss is transferred to comprehensive income.