Companies can passively own shares of securities as long as the investment ownership is less than 20%. These passive assets can be accounted for in different ways depending on how the firm decides to classify the investment.

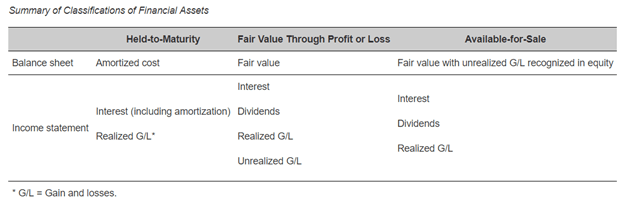

- Held-to-maturity. Held-to-maturity securities are debt securities acquired with the intent and ability to be held-to-maturity. The securities cannot be sold prior to maturity except in unusual circumstances. Long-term held-to-maturity securities are reported on the balance sheet at amortized cost. Amortized cost is the original cost of the debt security plus any discount, or minus any premium, that has been amortized to date. Amortized cost is simply the present value of the remaining cash flows (coupon payments and face amount) discounted at the market rate of interest at issuance. Interest income (coupon cash flow adjusted for amortization of premium or discount) is recognized in the income statement but subsequent changes in fair value are ignored.

- Fair value through profit or loss (held-for-trading or designated at fair value)

- Held-for-trading. Held-for-trading securities are debt and equity securities acquired for the purposes of profiting in the near term, usually less than three months. Held-for-trading securities are reported on the balance sheet at fair value. The changes in fair value, both realized and unrealized, are recognized in the income statement along with any dividend or interest income.

- Designated at fair value. Firms can choose to report debt and equity securities that would otherwise be treated as held-to-maturity or available-for-sale securities at fair value. Designating financial assets and liabilities at fair value can reduce volatility and inconsistencies that result from measuring assets and liabilities using different valuation bases. Unrealized gains and losses on designated financial assets and liabilities are recognized on the income statement, similar to the treatment of held-for-trading securities.

- Available-for-sale. Available-for-sale securities are debt and equity securities that are neither held-to-maturity nor held-for-trading. Like held-for-trading securities, available-for-sale securities are reported on the balance sheet at fair value. However, only the realized gains or losses, and the dividend or interest income, are recognized in the income statement. The unrealized gains and losses (net of taxes) are excluded from the income statement and are reported as a separate component of stockholders’ equity (in other comprehensive income). When the securities are sold, the unrealized gains and losses are removed from other comprehensive income, as they are now realized, and recognized in the income statement.