Costs of financial distress comprise of costs of bankruptcy and probability of financial distress. Costs can be direct, like increased expenses for bankruptcy expenses or indirect, like missing investment opportunities. Probability of financial distress is mostly from the sustainability of leverage, though poor management and governance can also play a role. Due to these high costs of distress, companies tend to minimize debt usage, all else equal.

Other factors of capital structure include agency costs of equity, costs of asymmetric information and the pecking order theory. Agency costs of equity refer to the costs associated with the conflicts of interest between managers and owners. Managers who do not have a stake in the company do not bear the costs associated with excessive compensation or taking on too much (or too little) risk. This leads to additional costs meant to minimize this cost, creating the net agency cost of equity, which includes monitoring costs, bonding costs and residual losses.

Costs of asymmetric information refer to costs resulting from the fact that managers typically have more information about a company’s prospects and future performance than owners or creditors. Firms with complex products or little transparency in financial statements tend to have higher costs of asymmetric information, which results in higher required returns on debt and equity capital. This will also lead shareholders and creditors to look for “signals” that may be indicators of management thinking. For example, issuing equity could be a signal of stock overvaluation while taking on debt could be a sign of strong cash flows to service the debt.

Pecking order theory, based on asymmetric information, is related to the signals management sends to investors through its financing choices. According to pecking order theory, managers prefer to make financing choices that are least likely to send signals to investors.

The pecking order (from most favored to least favored) is:

- Internally generated equity (i.e., retained earnings).

- Debt.

- External equity (i.e., newly issued shares).

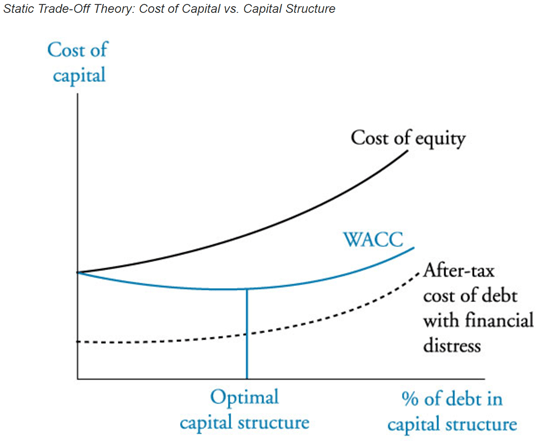

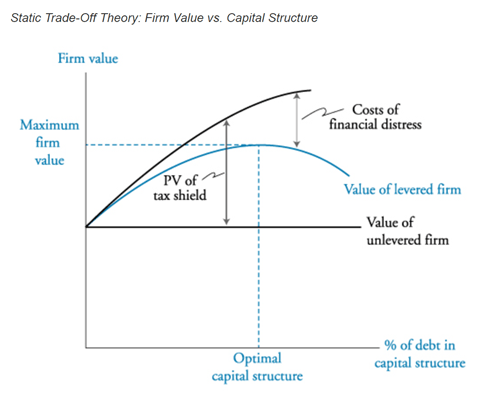

The Static Trade Off Theory

This theory builds on MM I and MM II by incorporate the cost of financial distress:

VL = VU + (t × d) − PV(costs of financial distress)

The after-tax cost of debt has an upward slope due to the increasing costs of financial distress that come with additional leverage. As the cost of debt increases, the cost of equity also increases because some of the costs of financial distress are effectively borne by equityholders. The optimal proportion of debt is reached at the point when the marginal benefit provided by the tax shield of taking on additional debt is equal to the marginal costs of financial distress incurred from the additional debt. This point also represents the firm’s optimal capital structure because it is the point that minimizes the firm’s WACC and therefore maximizes the value of the firm.