In free cash flow valuation models, we have a control perspective that assumers value recognition will be immediate. DDM models take a minority perspective which means that value may not be reflective of the DDM value until dividend policy correctly reflects long-run profitability.

Note that share repurchases, share issues and changes in leverage have little to no effect on FCFF and FCFE. Of the three, changes in leverage may lead to small changes in FCFE, everything else has no effect on FCFF and FCFE. A decrease in leverage through a repayment of debt will decrease FCFE in the current year and increase forecasted FCFE in future years as interest expense is reduced.

The single stage FCFF model is good for stable firms in mature industries. It is similar to the GGM.

The WACC is the weighted average of the rates of return required by each of the capital suppliers. Value of debt is adjusted for the tax rate. Subtract the market value of debt from the FCFF value before dividing.

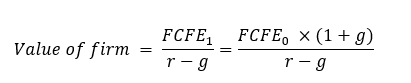

The single stage FCFE model is the same as the FCFF equivalent, but we use required return on equity instead of WACC:

The single stage model can be extended into multistage models if we are given various growth stages for a firm. The process of valuation is simply calculating the present value of the expected cash flows (which are projected according to the given growth stage) and adding that to a terminal value, which is basically the end state, single-stage value of the firm discounted back to present day. For example if a firm reaches its final growth state in year 3, the terminal value to be used will be:

We can also calculate the terminal value using valuation multiples such as the PE ratio.

terminal value in year n = (trailing P/E) × (earnings in year n)

terminal value in year n = (leading P/E) × (forecasted earnings in year n+1)