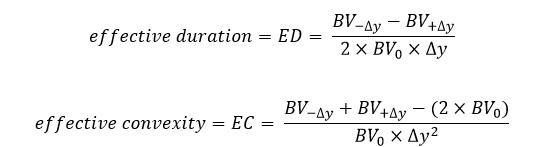

We cannot use modified duration and convexity measures on bonds with embedded options as there cash flows change if an option is exercised. Effective duration and effective convexity consider these potential changes in cash flows due to changes in interest rates.

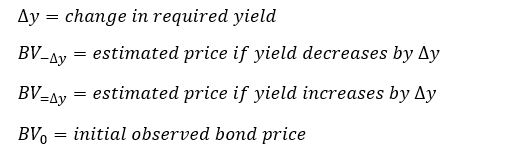

Where:

Calculating values of BV+Δy and BV–Δy is can be done using the following procedures:

- Given assumptions about benchmark interest rates, interest rate volatility, and any calls and/or puts, calculate the OAS for the issue using the current market price and the binomial model.

- Impose a small parallel shift in the benchmark yield curve by an amount equal to +Δy.

- Build a new binomial interest rate tree using the new yield curve.

- Add the OAS from step 1 to each of the one-year rates in the interest rate tree to get a “modified” tree.

- Compute BV+Δy using this modified interest rate tree.

- Repeat steps 2 through 5 using a parallel rate shift of –Δy to obtain a value of BV–Δy .