Active return measure the value that active management adds. It can be measure ex-ante, based on expectations, or ex-post, based on actual returns.

Ex-ante return = E(RA) = E(RP) − E(RB)

Where:

E(RP) = expected return of an actively managed portfolio

E(RB) = the expected return of active portfolio benchmark

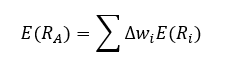

To identify the specific amount of value that active management added, we look at the active weights that made up the active return, comparing those weights to benchmark weightings. Overweighted securities have positive active weights, and underweighted securities have negative active weights. Active weights must sum to zero. We can create the following equation based on this:

Where:

When multiple assets classes are used, expected returns on the active and benchmark portfolios can be computed as the weighted average of securities returns:

Thus, the ex-ante active return is the expected return on the active portfolio minus the expected return on the benchmark:

Active return can also be broken down into two parts:

- Asset allocation return (from deviations of asset class portfolio weights from benchmark weights)

- Security selection return (from active returns within asset classes)