Traditional approaches to defining the investment opportunity set include classifying asset groups by liquidity or by how they perform over economic cycles.

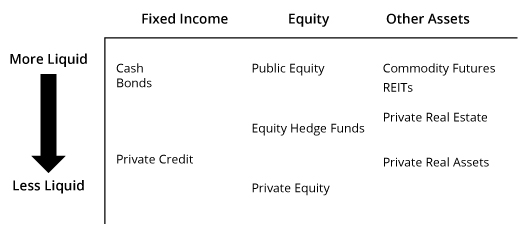

Liquidity-Based Investment Opportunity Set shows how asset classes might be considered based on liquidity characteristics.

Liquidity-Based Investment Opportunity Set

Opportunity Set shows an example of an investment opportunity set that uses this approach.

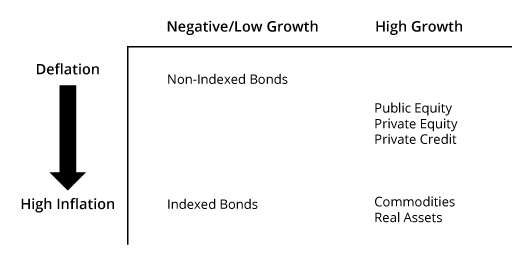

Economic Environment-Based Investment Opportunity Set

A risk factor based approach to defining asset classes involves statistically estimating their sensitivities to risk factors identified by the manager. Examples may include economic growth and inflation, interest rates and credit spreads, or currency values.

Main strengths of traditional approaches:

- Easy to communicate. Listing the roles of various asset classes is intuitive and easy to explain to the decision makers, who often have familiarity with the traditional asset class-based approach. Scenario analyses based on historical or expected behavior of various asset classes under different macroeconomic conditions can help to introduce quantitative aspects of the portfolio’s expected performance and risk and substantiate the asset allocation proposal.

- Relevance for liquidity management and operational considerations. Public and private asset class mandates have vastly distinct liquidity profiles. Thus, although private and public equity would have a lot of commonality in their risk factor exposures, they would be positioned very differently from a liquidity management perspective. Similarly, investors must implement the target asset allocation by allocating to investment managers. The traditional categorization of asset classes may be necessary to identify the relevant mandates—what portion of the equity portfolio she would like to allocate to equity-oriented hedge funds rather than to long-only equity managers.

Main limitations of traditional approaches:

- Over-estimation of portfolio diversification. Without a proper analytical framework for assessing risk, investors may have a false sense of diversification. An allocation spread across a large number of different asset classes may appear to be very well diversified, when, in fact, the underlying investments may be subject to the same underlying risks.

- Obscured primary drivers of risk. Investments with very different risk characteristics may be commingled under the same asset class category. For example, government bonds and high-yield bonds may both be classified as “fixed income,” but each has distinct risk characteristics.

Risk-based approaches are designed to overcome some of these limitations.

Key benefits of risk-based approaches:

- Common risk factor identification. Investors are able to identify common risk factors across all investments, whether public or private, passive or active.

- Integrated risk framework. Investors are able to build an integrated risk management framework, leading to more reliable portfolio-level risk quantification.

Key limitations of risk-based approaches:

- Sensitivity to the historical look-back period. Empirical risk factor exposure estimations may be sensitive to the historical sample.

- Implementation hurdles. Establishing a strategic target to different risk factors is a very important high-level decision, but converting these risk factor targets to actual investment mandates requires additional considerations, including liquidity planning, time and effort for manager selection, and rebalancing policy.