Business cycles are fluctuations in economic activity that follow a wave like pattern. While generally simplified into a single wave, it is more accurate to think of the broad market business cycle as made up of many smaller cyclical components of economic activity. The variance in these underlying components makes each individual business cycle unique.

Business cycles arise from decisions that:

- are made based on imperfect information or uncertain expectations of future value,

- require structural processes to implement (long time horizon)

- are difficult and/or costly to reverse (sunk cost)

There are 5 stages of the business cycle.

- Initial Recovery

- Early Expansion

- Late Expansion

- Slowdown

- Contraction

Each stage of the cycle has unique economic and capital market implications. We will consider each stage of the cycle terms of the expected yield curve, inflation expectations and capital asset values.

Initial recovery – Characterized by improving business confidence and economic conditions. A large output gap and low consumer confidence still exists from the previous contraction. Recovery is often supported by an upturn in spending on housing and consumer durables. Increase in inventories.

- Typical Duration – a few months

- Government policy – Will be stimulative, low interest rates, running budget deficits. High nominal rates are expected.

- Yield curve – Yield curve is steep at the bottom of a cycle. Short term rates will be falling or low, long term rates bottom.

- Inflation – Inflation will be very low, may be decelerating/declining at outset of phase.

- Asset Prices – Low yields means bonds will be peaking, barring expectations of disinflation. Stocks will start to rally, riskier assets (SC/HY/EM) will outperform. Cash equivalents will earn nominal interest rate and can be attractive in the face of rising rates. Real Estate likely still stable.

Early Expansion – Characterized by an economy that continues to improve. Confidence rises. Unemployment fall though output gap still likely negative. Consumer spending and borrowing rises, business production and investments rise. Profits typically rise rapidly. Demand for housing and consumer durables is strong.

- Typical Duration – year to several years

- Government policy – Stimulus will start to be withdrawn. If monetary/fiscal withdrawn at different paces, mid nominal rates expected from mixed policy.

- Yield curve – Curve remains steep though may begin to flatten. Short term rates will tend to rise first, while long term yields may be stable. (Front steepens, back-half flattening)

- Inflation – Inflation will be low.

- Asset Prices – Bond prices may begin to decline, depending on how stable YC is. Definitely have peaked. Stocks will continue to grow.

Late Expansion – Characterized by an economy that is approaching/will be at full strength. Output gap will be closed. Low employment, wage growth is strong. Confidence is high, balance sheets expand with leverage.

- Government policy – Policy will begin to be restrictive. If policy is mixed, mid-nominal rates is expected.

- Yield curve – Curve will flatten. Yields will increase overall, though short term increase may have faster pace, leading to the flattening. (Flattening from long inwards)

- Inflation – Inflation will be increasing.

- Asset Prices – Bond prices will decline as curve will be rising across the board. Stock prices will still be increasing, though with increasing volatility. Will likely peak during this stage of the cycle. Inflation hedged assets like commodities may outperform. Cash can be seen as inflation hedge, will earn the short term interest rate.

Slowdown – Characterized by an economy that is showing signs of slowing. Business confidence will drop, along with inventories. High debt levels, few investment opportunities.

- Typical Duration – few months to a year or longer

- Government policy – Tight policy. Low expected nominal yields.

- Yield curve – Yield curve will be flat to inverted at points during this phase. Short-term rates will be approaching or at peak, long-term yields will have peaked.

- Inflation – Inflation will continue to accelerate.

- Asset Prices – Bond prices will bottom or start to increase. Long bonds will show stronger movement. Credit spreads generally widen. Stock prices will be soft or decline.

Contraction – Characterized by an economy that is in recession. Large drop in economic activity. Drops in business investment, inventories due to fewer sales. Consumer and business confidence decline. Tightening credit magnifies downward pressure on the economy. Recessions are often punctuated by major bankruptcies, incidents of uncovered fraud, exposure of aggressive accounting practices, or a financial crisis. Unemployment can rise quickly, impairing household financial positions.

- Typical Duration – 12 to 18 months

- Government policy – Progressive loosening, aiming to create a “soft-landing.”

- Yield curve – Yield curve will start steepening as short term yields drop faster than long term yields. However, yields will decrease overall. Will be steepest again on cusp of recovery.

- Inflation – Inflation will peak.

- Asset Prices – Bond prices will increase. Stock prices decline, though will bottom before end of this phase.

Inflation also can have a subset of impacts on asset values based on whether the realized levels are expected or a surprise:

| Inflation within expectations | Cash equivalents: Earn the real rate of interest Bonds: Shorter-term yields more volatile than longer-term yields Equity: No impact given predictable economic growth Real estate: Neutral impact with typical rates of return |

| Inflation above or below expectations | Cash equivalents: Positive (negative) impact with increasing (decreasing) yields Bonds: Longer-term yields more volatile than shorter-term yields Equity: Negative impact given the potential for central bank action or falling asset prices, though some companies may be able to pass rising costs on to customers Real estate: Positive impact as real asset values increase with inflation |

| Deflation | Cash equivalents: Positive impact if nominal interest rates are bound by 0% Bonds: Positive impact as fixed future cash flows have greater purchasing power (assuming no default on the bonds) Equity: Negative impact as economic activity and business declines Real estate: Negative impact as property values generally decline |

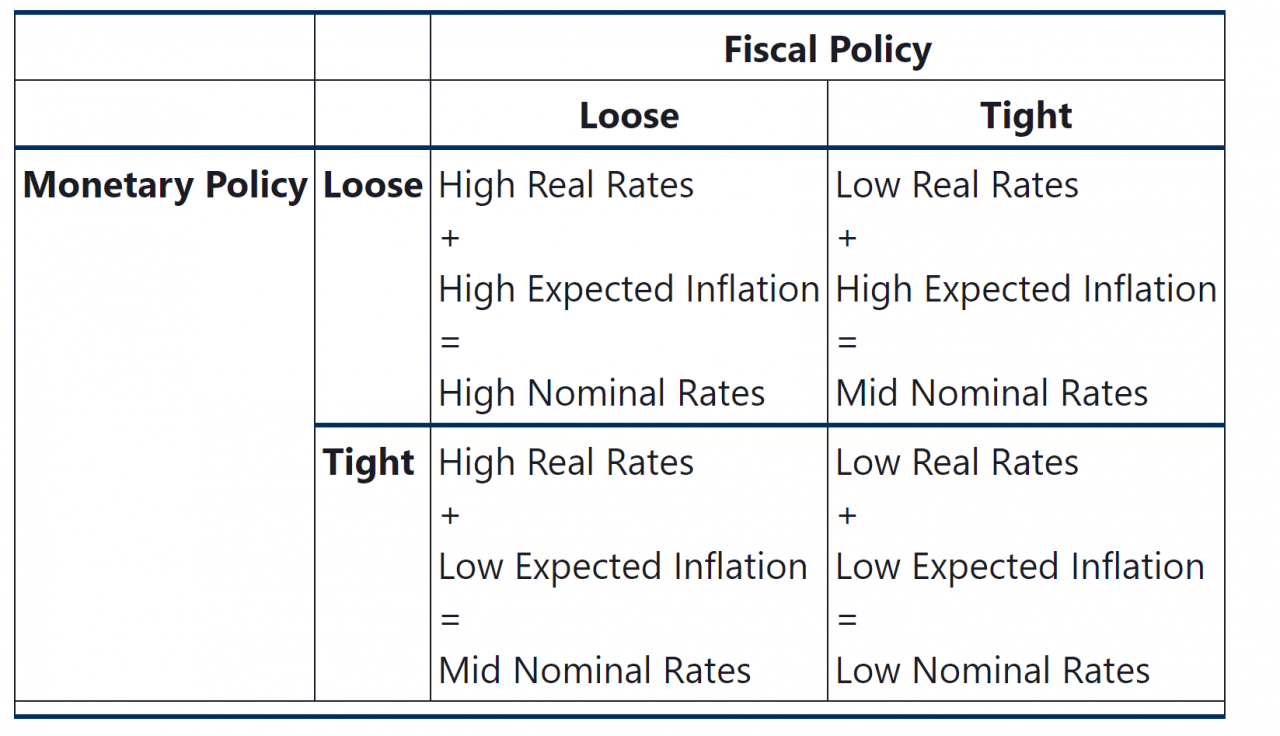

Fiscal and monetary policies may reinforce or conflict with each other. If the policies reinforce each other, the implications for the economy are clear. In all other cases, there are likely implications for the yield curve:

- If both policies are stimulative, the yield curve is steep and the economy is likely to grow.

- If both policies are restrictive, the yield curve is inverted and the economy is likely to contract.

- If monetary policy is restrictive and fiscal policy is stimulative, the yield curve is flat and the implications for the economy are less clear.

- If monetary policy is stimulative and fiscal policy is restrictive, the yield curve is moderately steep and the implications for the economy are less clear.